- Randall Bartlett

Deputy Chief Economist

Economic News

Canada: There Was a Lot to Like in May’s Modest Inflation Advance

June 24, 2025

Highlights

- Headline CPI rose 1.7% y/y in May, matching the advance in April as well as the consensus expectation of economists. Prices edged up 0.6% month-over-month and rose 0.2% after adjusting for seasonal effects. Table 1 summarizes the key data points.

Comments

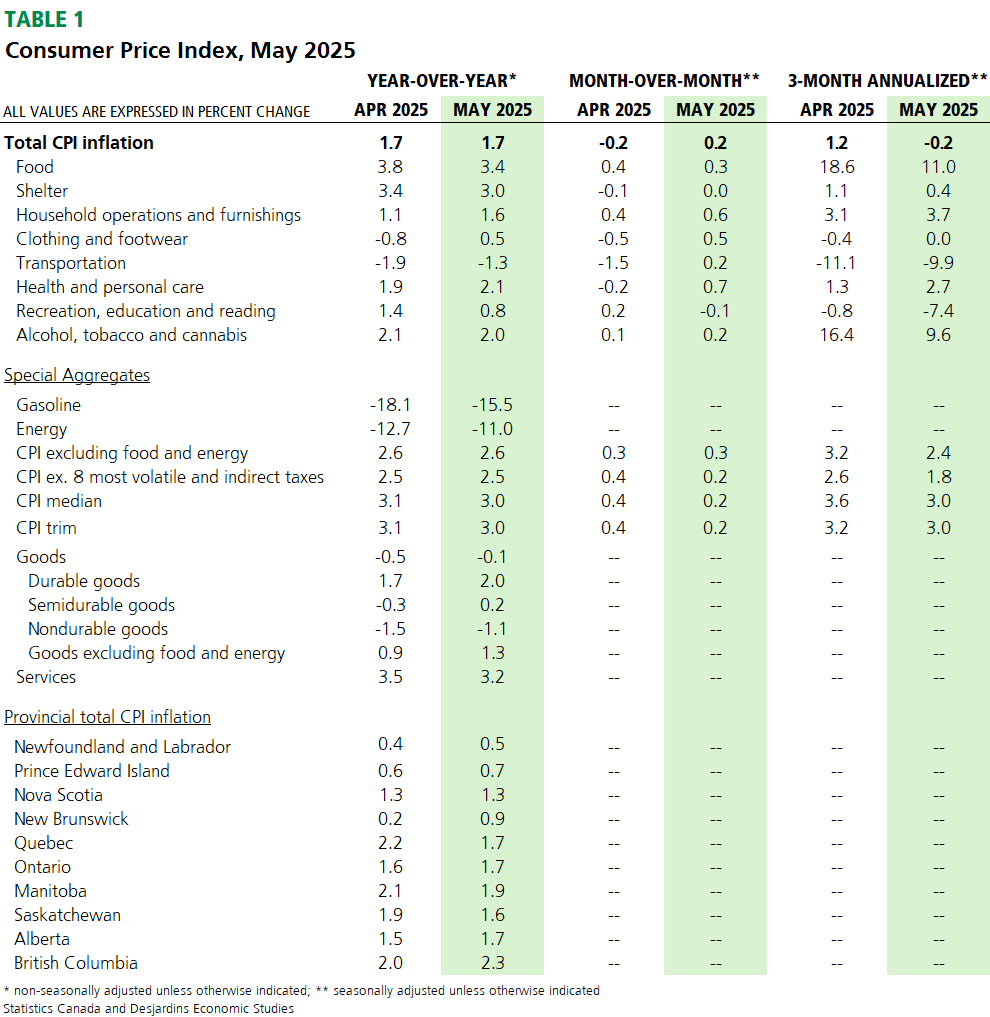

At 1.7% y/y in May, headline inflation came in below the Bank of Canada’s (BoC’s) 2% inflation target for the second consecutive month. Lower energy price growth, largely because of the elimination of the federal consumer carbon tax in April, was again the primary reason of the modest year-over-year total CPI advance (graph 1). Our analysis External link. suggests headline inflation would be as much as 0.7 percentage points higher if not for this tax change, and that the resulting drag on price growth should persist through to April of next year (see our forecast External link.).

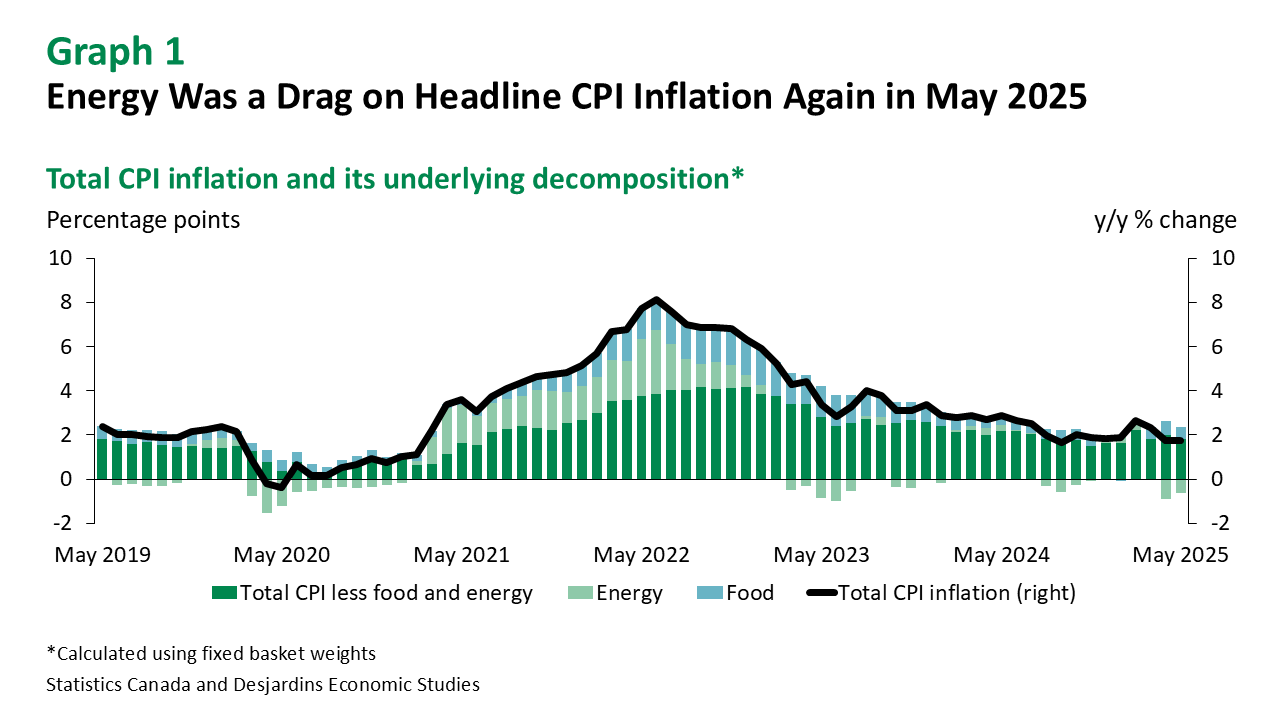

But the good news in May didn’t stop with energy prices. While still elevated, food inflation also slowed in the month (graph 2). So did shelter inflation, as rent inflation reversed its April uptick and mortgage interest cost decelerated for the 21st consecutive month. The remaining inflation categories slowed on average in May as well. This despite the inflationary impacts of retaliatory tariffs that are no doubt playing a role in pushing the price of household operations and furnishings, as well as clothing and footwear, higher (see our analysis External link.).

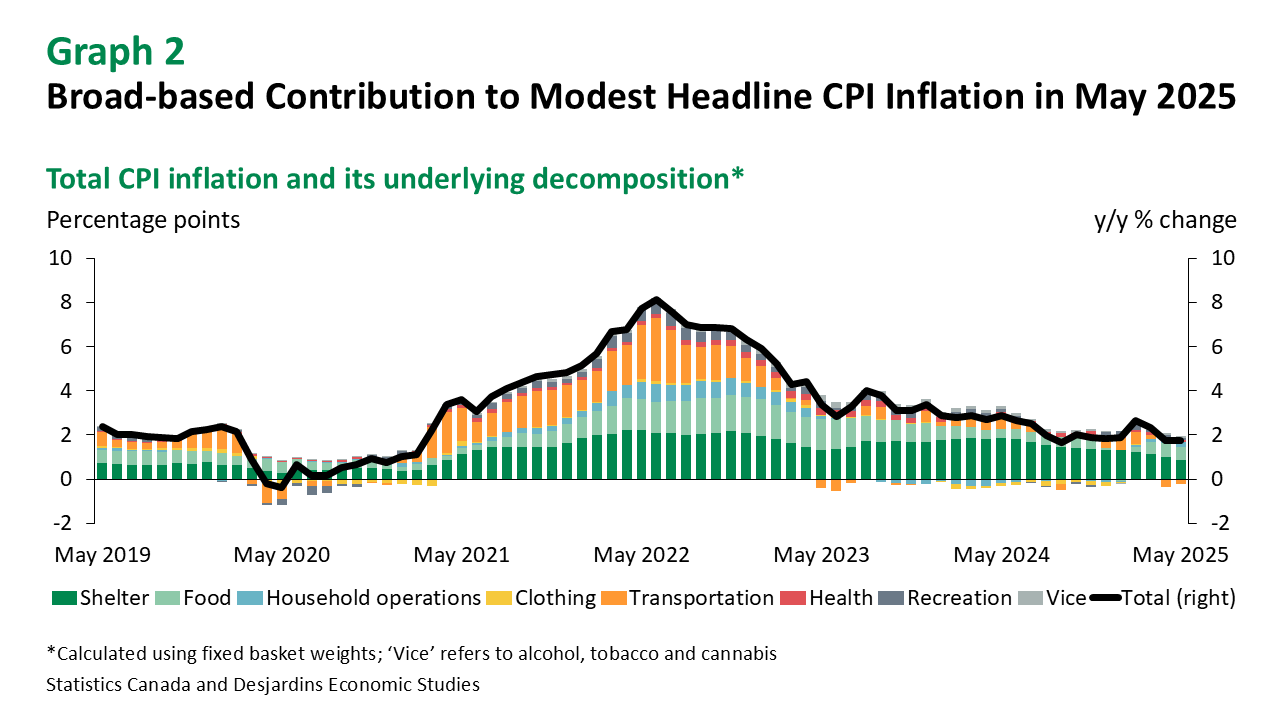

The BoC’s preferred measures of core inflation—CPI median and trimmed mean—also pointed to a cooling in underlying price growth in May. On a year-over-year basis, they advanced by an average of 3.0% y/y from a recent high of 3.1% in April. The annualized 3-month moving average of these core seasonally adjusted series moved lower in May as well. (Of note, these measures do not incorporate the effect of the carbon tax cut, unlike headline CPI.) Other measures of near-term underlying inflation slowed even that much more in the month, and are well down from their February 2025 multi-year peak (graph 3). This suggests the bounce in core inflation in April may have been short lived.

Implications

The May 2025 inflation print was good all around. Of concern for the BoC at its June meeting External link. was the recent reacceleration in core inflation measures. Our view was that this boost was temporary, and the turn in underlying inflation in May suggests that assertion may be correct. And with headline inflation below 2% and likely to remain low for the next year as a result of the elimination of the consumer price on pollution and weaker growth External link., inflation expectations should start to come down. If they do, this will give the Bank of Canada even more room to ease policy than it might have had otherwise. Consequently, after leaving the policy rate unchanged in June due to the uncertainty of the tariff-impacted economic outlook and accelerating core inflation, we think the BoC will resume cutting at its July meeting.