- Randall Bartlett

Deputy Chief Economist

Economic News

Canada: Higher Core Inflation in June Should Keep the BoC on the Sidelines for Now

July 15, 2025

Highlights

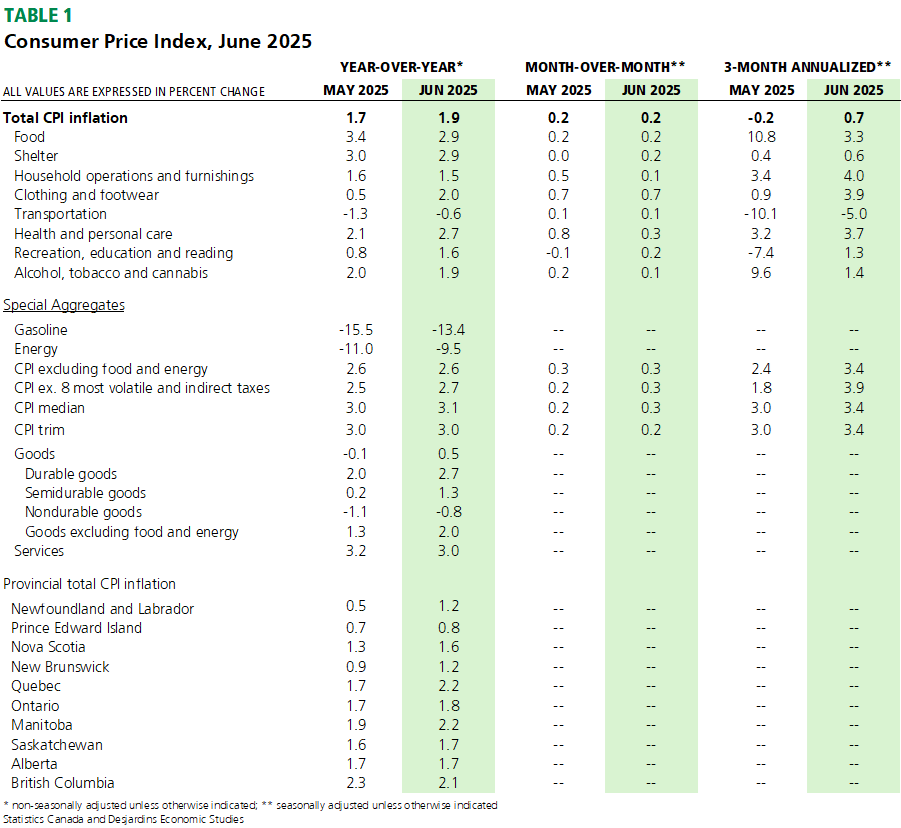

- Headline CPI rose 1.9% y/y in June, up from 1.7% y/y in May and in line with the consensus expectation of economists. Prices edged up 0.1% month-over-month and rose 0.2% after adjusting for seasonal effects. Table 1 summarizes the key data points.

Comments

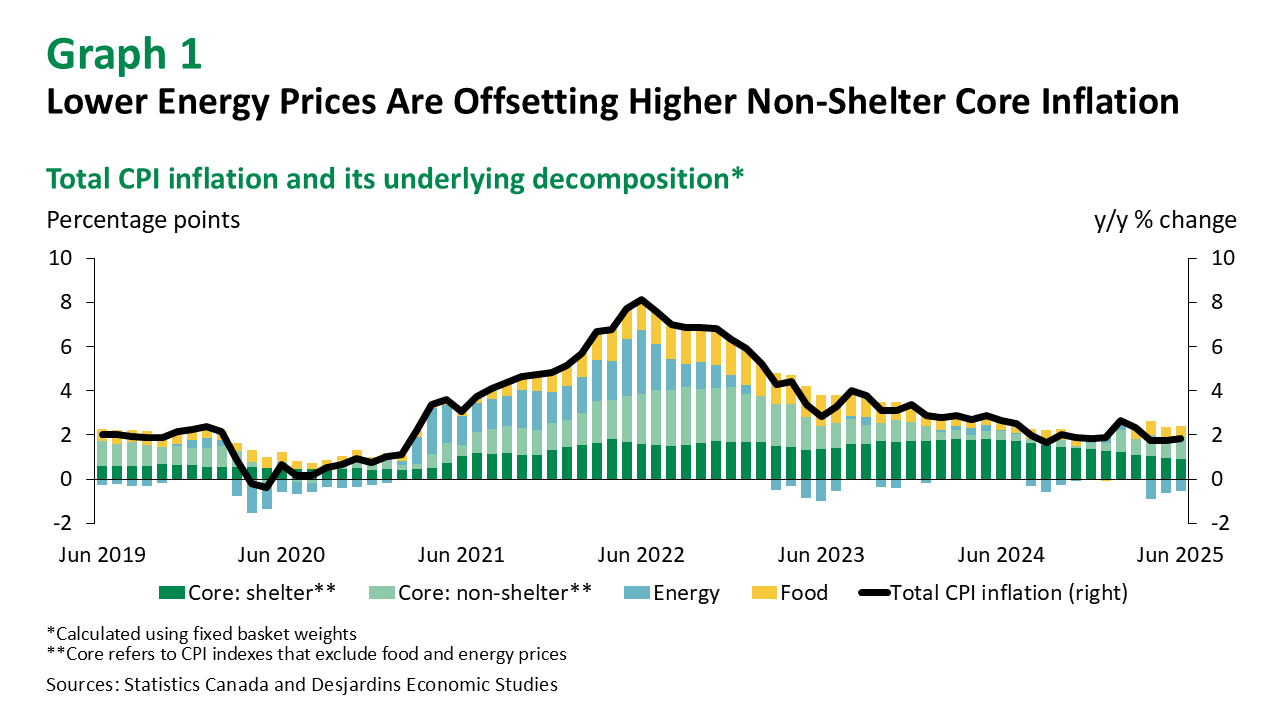

Headline inflation came in below the Bank of Canada’s (BoC’s) 2% inflation target for the third consecutive month in June, clocking in at 1.9% y/y. Lower energy prices than a year ago, largely because of the elimination of the federal consumer carbon tax in April, were again the primary reason (graph 1). (See our analysis External link. for more information.)

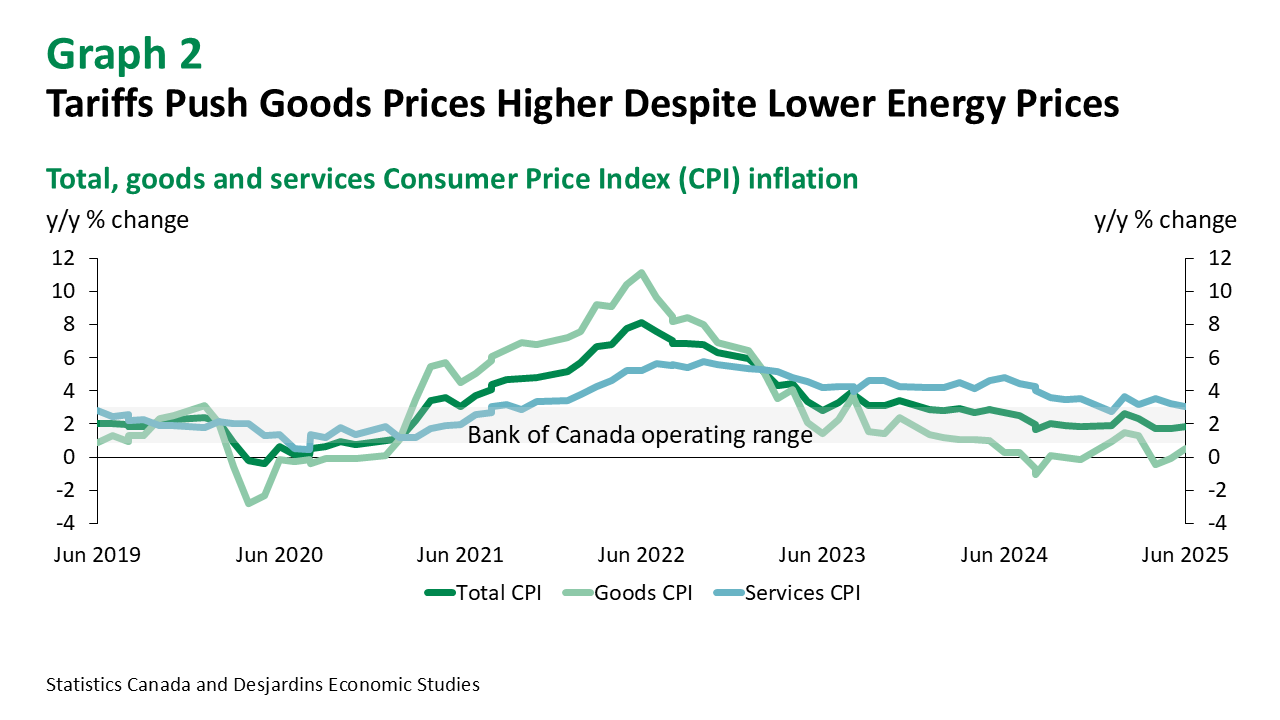

While lower energy prices may have eased June inflation, other goods saw notable price gains. The price of food purchased from stores increased 2.8% y/y from a year earlier, albeit slowing from May due to a sharp drop in some fresh vegetable prices. In contrast, durable goods prices accelerated (to 2.7% from 2.0% in May), driven by higher prices for passenger vehicles (4.1%) and furniture (3.3%). In the case of passenger vehicles, new vehicle sales have been strong since the start of the year, likely to get ahead of tariffs. That, in combination with the pause in the federal electric vehicle rebate, are likely culprits behind the new-vehicle price index now running at 5.2% y/y. By contrast, new-vehicle prices only grew by 0.2% y/y in the US in June. Prices of clothing and footwear also rose in the month. Consequently, goods price inflation turned positive for the first time since March (graph 2), hitting 2.0% y/y when excluding the prices of energy and food purchased from stores. Statistics Canada chalked some of the acceleration in June goods inflation to higher costs resulting from the trade war (see our analysis External link.). But even this pales in comparison to services inflation which, at 3.0% in June, has had a three-handle in it in every month but one since August 2021.

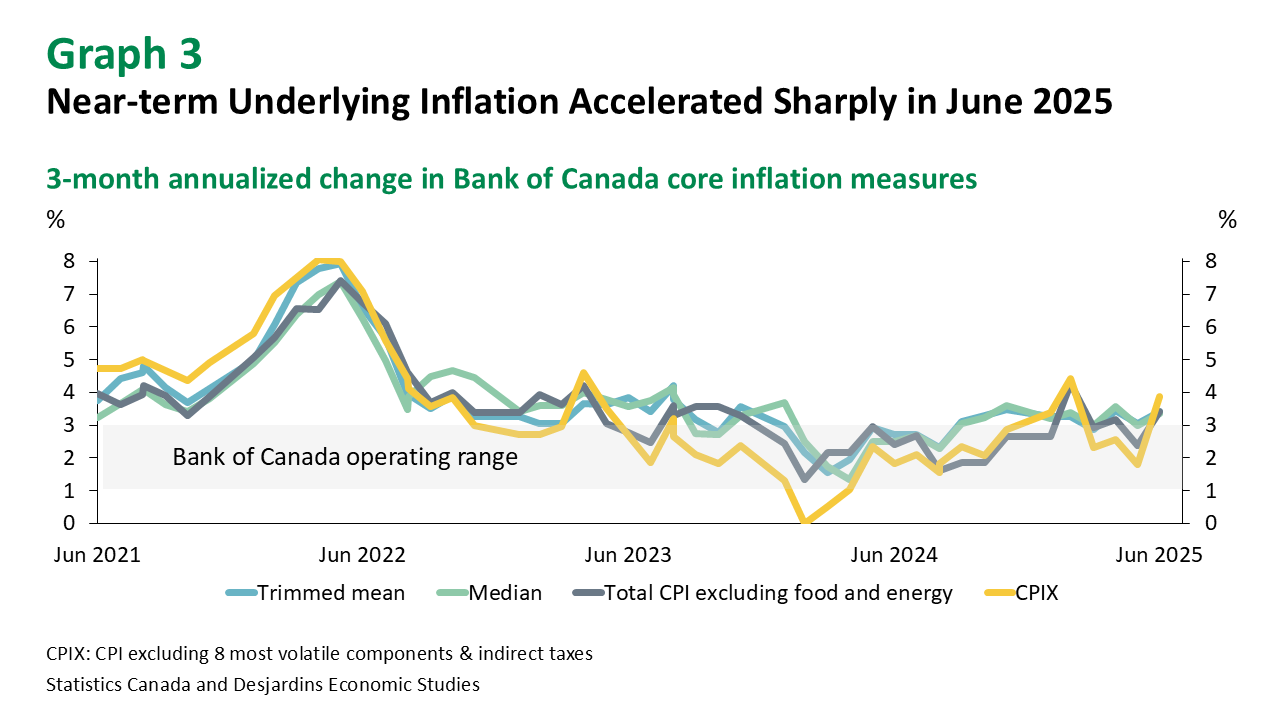

But core CPI inflation stole the spotlight in June, with the BoC’s preferred measures of core inflation—CPI median and trimmed mean—edging up to 3.1% and 3.0%, respectively. The annualized 3-month moving average of these measures jumped to 3.4% in June from 3.0%, undoing the improvement made in May. Other near-term inflation indicators accelerated, reaching to their highest levels since February 2025 (graph 3). This suggests the reprieve in underlying inflation in May could have been short lived.

Implications

Despite signs of an economic slowdown due to trade tensions with the United States, we expect the Bank to put more focus on recent employment gains and, to a larger degree, the rebound in core inflation. As such, the BoC is likely to keep rates steady at its upcoming meeting at the end of the July. However, with economic storm clouds still on the horizon, we are of the view that the Bank will resume cutting interest rates in September.