- Randall Bartlett

Deputy Chief Economist

Economic News

Canada: Lower Energy Prices Weighed on April Inflation, but That’s Where the Good News Ends

May 20, 2025

Highlights

- Headline CPI rose 1.7% y/y in April, slowing considerably from a 2.3% advance in March and coming in a tick higher than the consensus expectation of economists (1.6%). Prices edged 0.1% m/m lower month-over-month, and fell 0.2% after adjusting for seasonal effects. Table 1 summarizes the key data points.

Implications

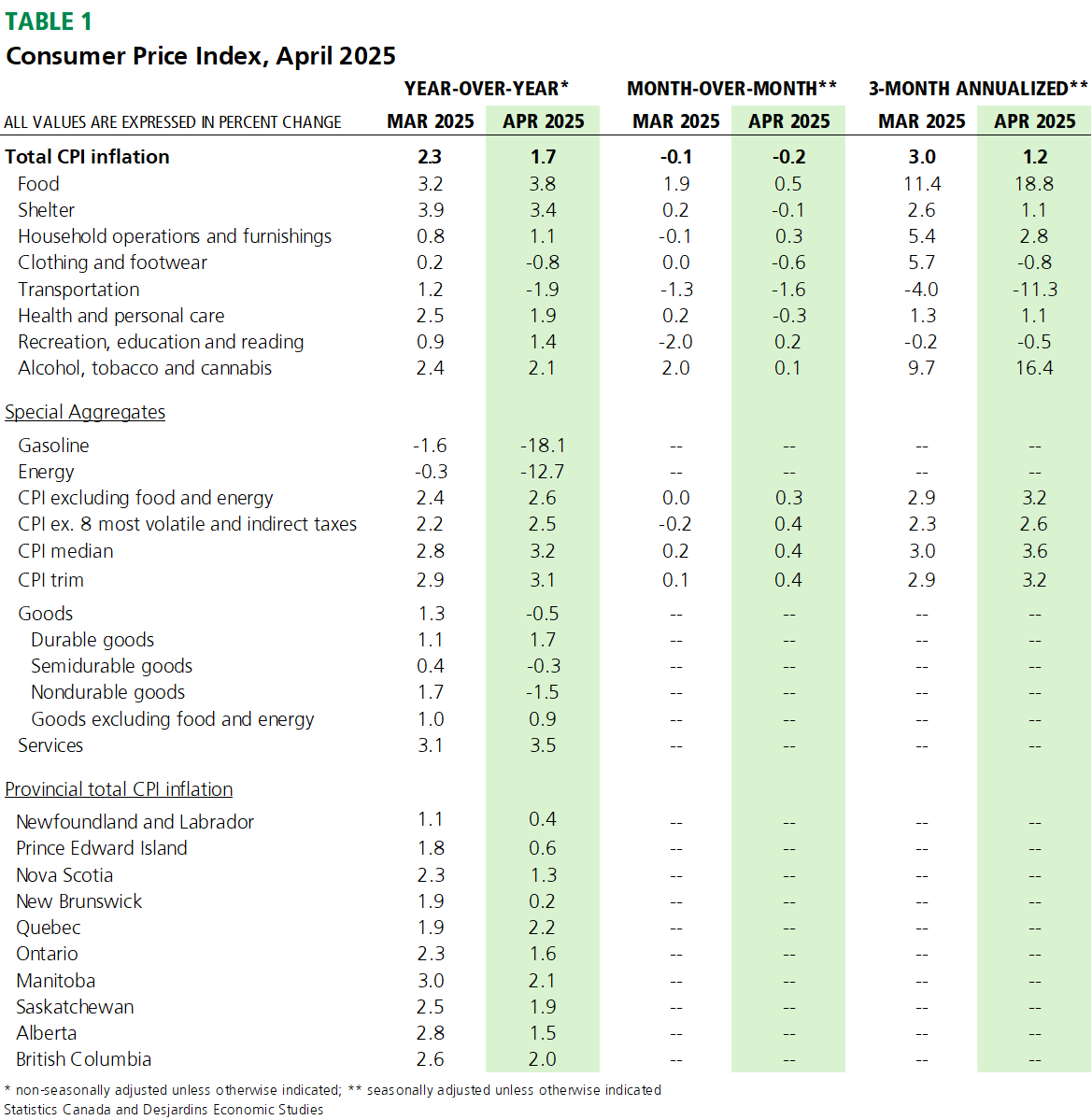

The sharp deceleration in inflation in April can almost entirely be chalked up to a drop in energy prices because of the elimination of the federal price on pollution. Gasoline prices saw the largest contraction among the energy CPI constituent series, but prices of fuel for recreational vehicles and natural gas weren’t far behind (graph 1). Our analysis External link. suggests headline CPI inflation would have been about 0.7 percentage points higher in April if not for this tax change.

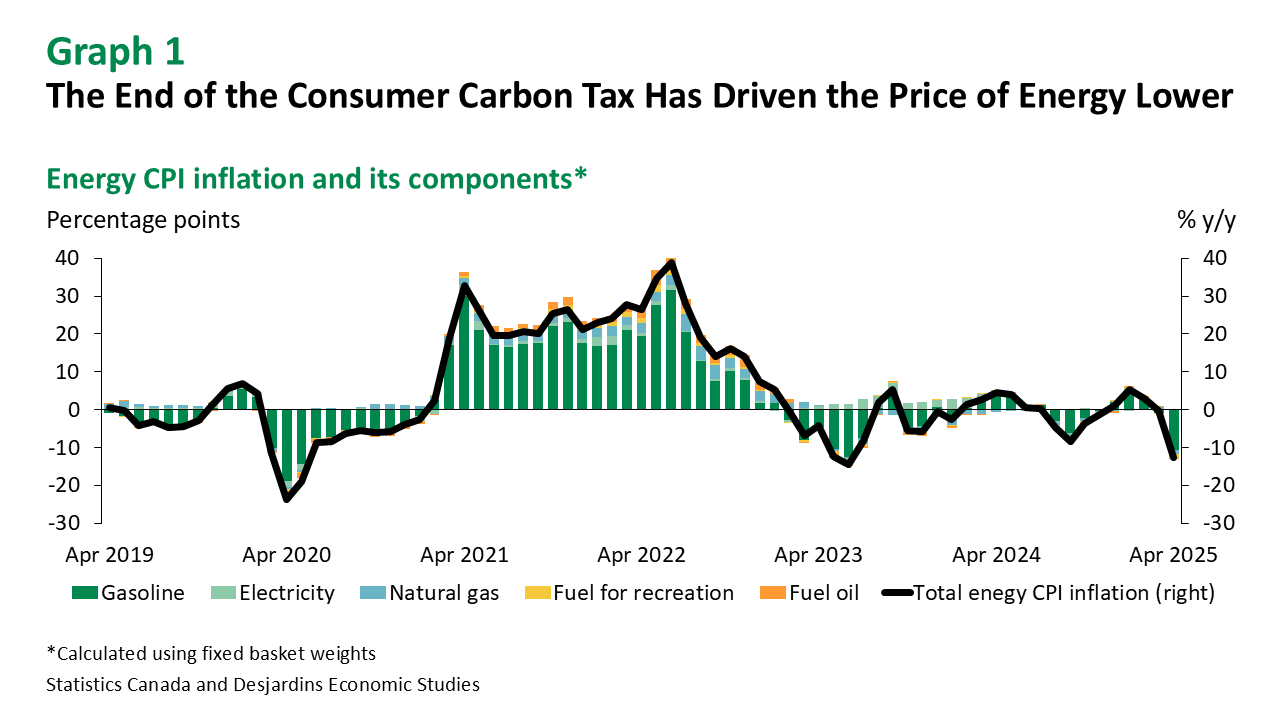

In contrast, food inflation continued to accelerate in the month (graph 2). So did core non-shelter inflation, as the price of things like travel tours and household equipment moved higher. The imposition of retaliatory tariffs and Canadian dollar weakness at the time no doubt played a role. Core shelter inflation slowed modestly again in April.

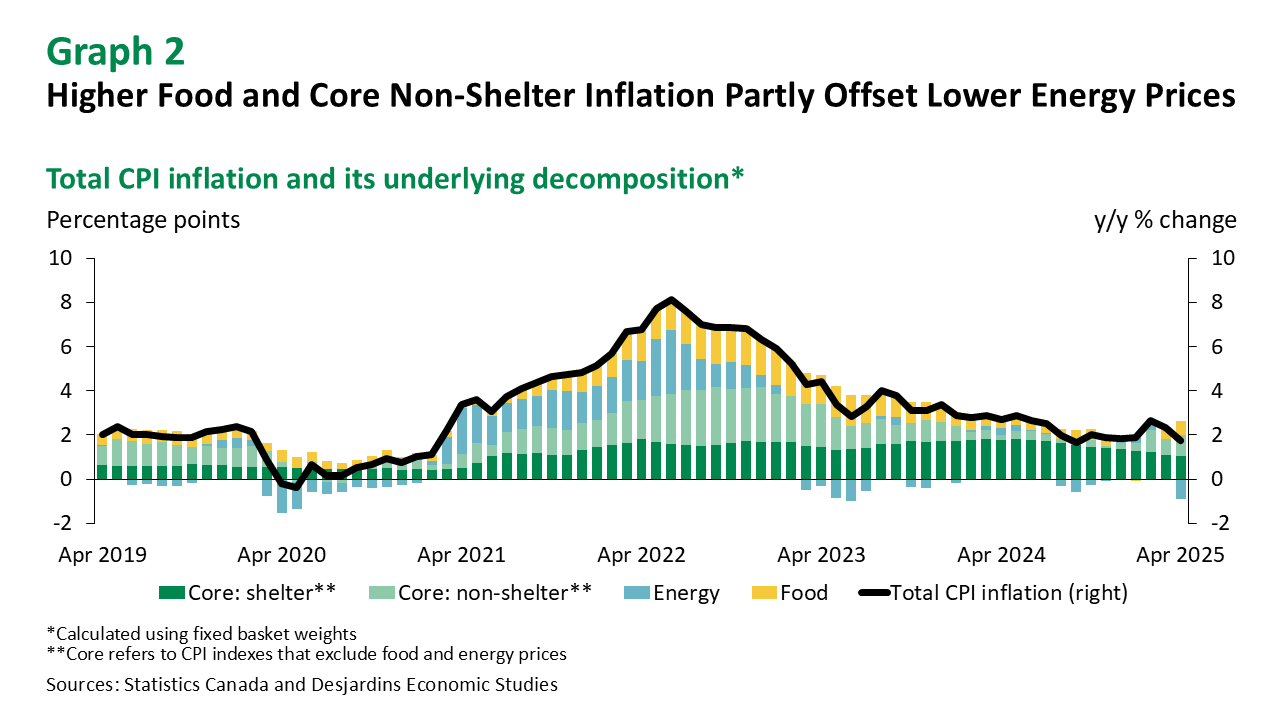

The Bank of Canada’s (BoC’s) preferred measures of core year-over-year price growth—CPI median and trimmed mean—jumped in April to an average of 3.2% y/y from 2.9% in March (graph 3). Of note, these measures do not incorporate the effect of the carbon tax, unlike the headline measure. The annualized 3-month moving average of these seasonally adjusted series moved even that much higher from the previous month’s pace. This suggests the reprieve in underlying inflation in March may have been short lived.

The April 2025 inflation print was not as good news as the headline number may suggest. But with inflation below 2% and likely to remain low for the next year thanks to the elimination of the price on pollution, inflation expectations should start to come down. If they do, this will give the Bank more room to cut interest rates than it might have had otherwise. And this despite the inflationary impacts of retaliatory tariffs and a lower Canadian dollar likely more than offseting the tariff-induced drag from a weaker economy on price growth (see our analysis).

All told, we expect the Bank of Canada to cut the policy rate by another 25 basis points at its upcoming June rate announcement, bringing the overnight rate to 2.50%. The recent pull back in bilateral US-China tariffs benefit Canada’s economy from higher external demand than might have otherwise been the case. Canada will hope to extract further concessions from the US administration, particularly on tariffs affecting auto assembly, steel, aluminum and lumber. Successful negotiations would minimize the stagflationary shock here at home. This recent positive tailwind to the outlook should reduce the likelihood of a 50 basis point cut in June, and we now forecast a terminal overnight rate of 2.00%, up from 1.75%.