- Randall Bartlett

Deputy Chief Economist

Economic News

Canada: December Inflation Came Down but Uncertainty Abounds

January 21, 2025

Highlights

- Headline CPI rose 1.8% y/y in December, down one tick from November and similarly below the expectations of economists (1.9%). Prices were down 0.4% month-over-month following a flat print in November, but moved up 0.2% after adjusting for seasonal effects. Table 1 summarizes the key data points.

Implications

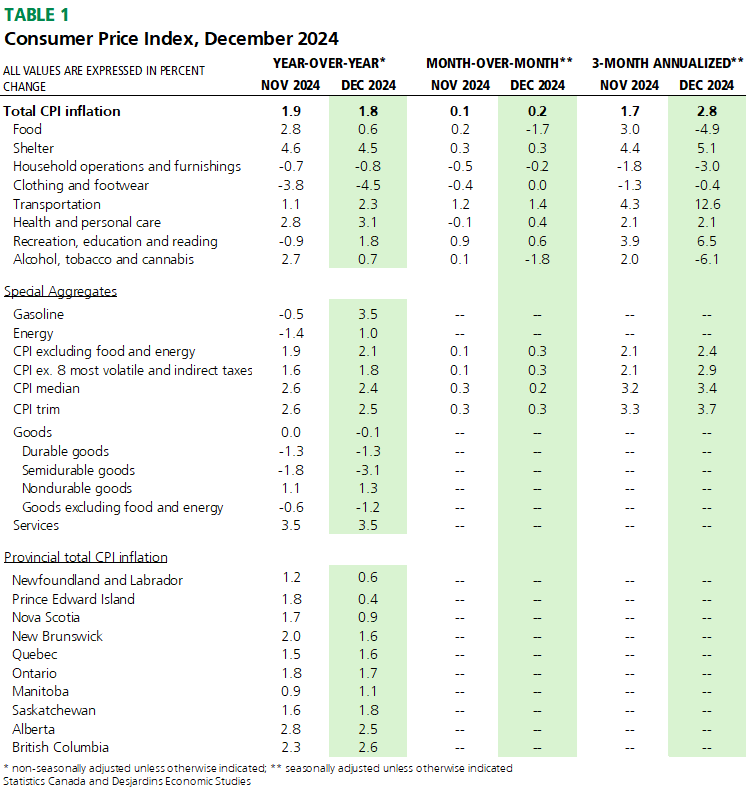

Another month, another inflation print at or below the Bank of Canada’s 2% target. The two-month GST/HST holiday played an important role this time around, with the mid-month start weighing on prices. Food purchased from restaurants contributed the most to the deceleration, leading food CPI inflation to slow to 0.6% from 2.8% in November (graph 1). On a month-over-month basis, food prices fell 1.8% m/m in December. Other CPI categories also posted notable declines in the month because of the GST/HST holiday, including alcohol purchased from stores (-1.3% y/y); prices for toys, games (excluding video games) and hobby supplies (-7.2%); and children's clothing (-10.6%). This drag helped to offset a reacceleration in prices of energy (up 1.0%, from -1.4% in November) and other non-energy or food inflation categories, such as travel services (7.9%). Indeed, the CPI excluding food rose 2.1% in December over a year earlier.

While the sales tax holiday helped to push goods inflation lower by a tick in December (-0.1% y/y), services prices held steady (3.5%) after slowing in each of the prior five months. Shelter inflation continues to make by far the largest contribution headline inflation (graph 2), but slowed for the ninth month in a row to 4.5%. While the rented accommodation CPI advanced by 6.9%, it’s the slowest advance since August 2023, and our research External link. suggests it should slow steadily going forward. At the same time, the weightier owned accommodation inflation slowed to 4.5%—a pace not seen since May 2021—thanks to the sustained slowdown in mortgage interest cost (11.7%) and drag from homeowners’ replacement cost (0.0%).

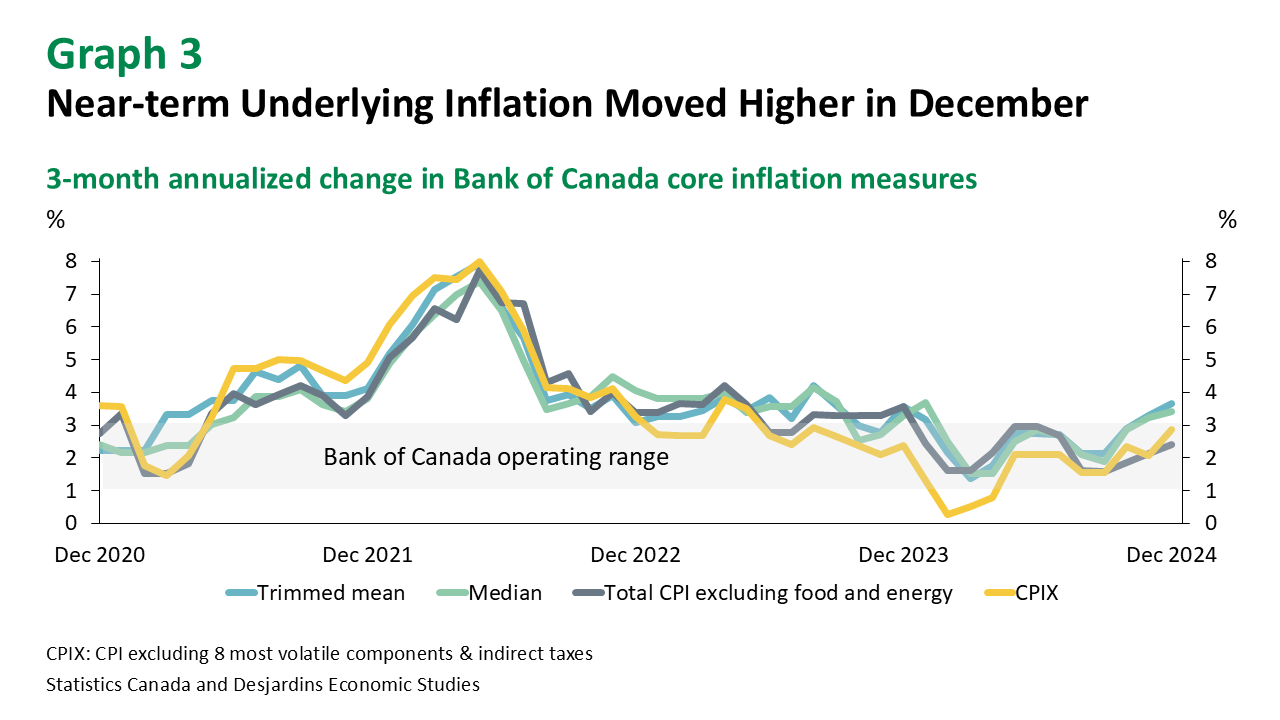

Looking to underlying inflation, the Bank of Canada’s preferred measures of core year-over-year price growth—CPI median and trimmed mean—decelerated in December (averaging 2.5% y/y) to the slowest pace in three months. However, the annualized 3-month moving average of these seasonally adjusted series moved higher again in December, topping 3% for the second month in a row (graph 3). However, other measures of underlying inflation also accelerated in the month, suggesting the advance in underlying inflation observed last month may be more than just an aberration.

While the further deceleration in headline CPI inflation was a positive in December, this is muddied by the GST/HST holiday that started in the month. January and February CPI readings will be similarly distorted (see our analysis External link. on the inflation implications). Indeed, the drag from lower sales taxes will offset some of the base effects that were expected to push inflation materially higher in Q1 2025, thereby keeping inflation at the start of the year close to the Bank’s 2% target. At the same time that inflation is coming in around the Bank’s target, we’re tracking Q4 real GDP growth above the BoC’s latest forecast of 2.0% annualized, suggesting all is relatively well on the home front. But with the inauguration of President Donald Trump yesterday, downside risks to the economy abound External link., not least from the threat of a 25% tariff being introduced on February 1. This economic uncertainty reinforces our call the next rate cut in January is likely to be a modest 25 basis points, and that subsequent rate reductions should be of a similar magnitude.