- Florence Jean-Jacobs

Principal Economist

Economic News

Bracing for the Storm? Businesses Posted Muted Profits but Resilient Non-Residential Investment in Q1

May 30, 2025

Highlights

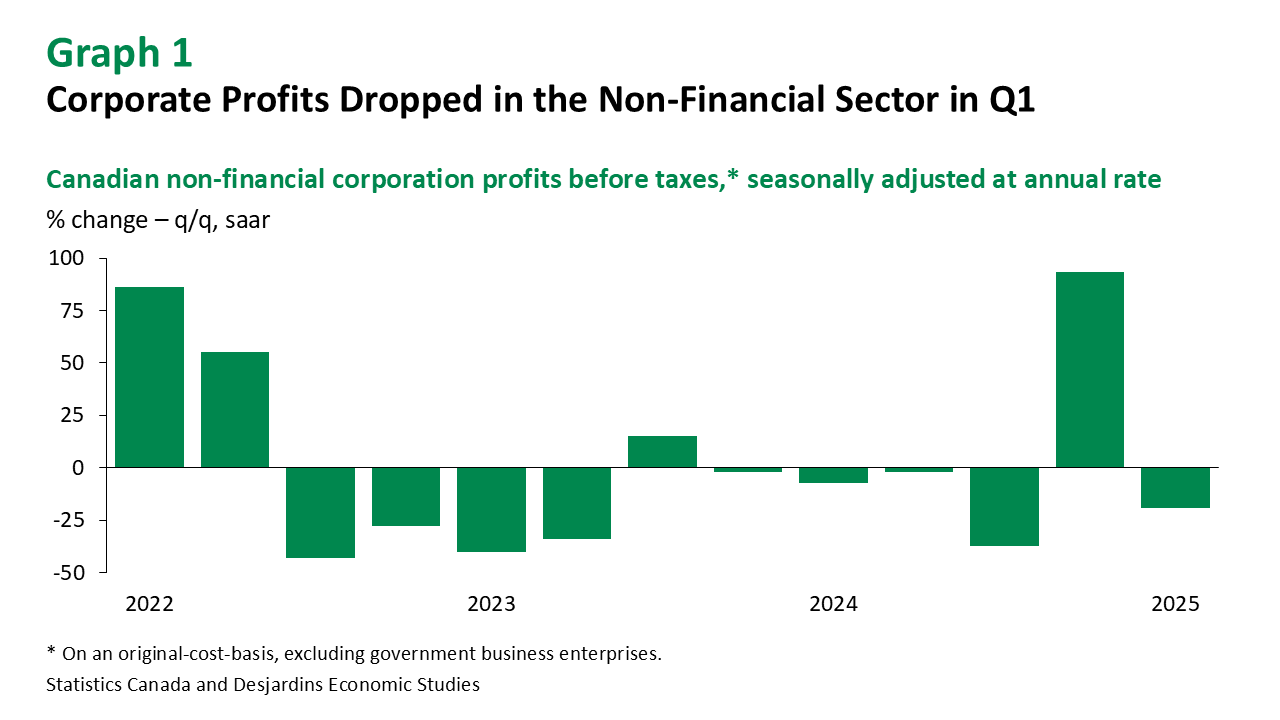

- Profits of Canadian non-financial corporations dropped 19.1% q/q annualized in the first quarter of 2025 (graph 1). According to Quarterly Financial Statistics released last week, declining profits in certain manufacturing sectors explain the disappointing net income results in Q1. Notably, motor vehicle manufacturers posted lower net income before tax (NIBT), down by over 50% annualized compared to both the previous quarter and the same quarter last year. A sizeable drop was also recorded in the alcoholic beverage, tobacco and cannabis product manufacturing – a result linked to one-time expenses in legal settlements. Pharmaceutical products also recorded a drop in profits.

- This weakness is despite higher energy prices in January and heightened export activity boosting revenues in the oil and gas extraction industry. Other energy-related sectors saw rising profits: petroleum and coal product manufacturing posted the second-largest increase in NIBT in Q1, after oil and gas extraction. This follows four consecutive quarterly declines. Pipeline transportation also recorded higher profits, as tariff uncertainty likely drove businesses in this sector to increase their activity before tariffs hit.

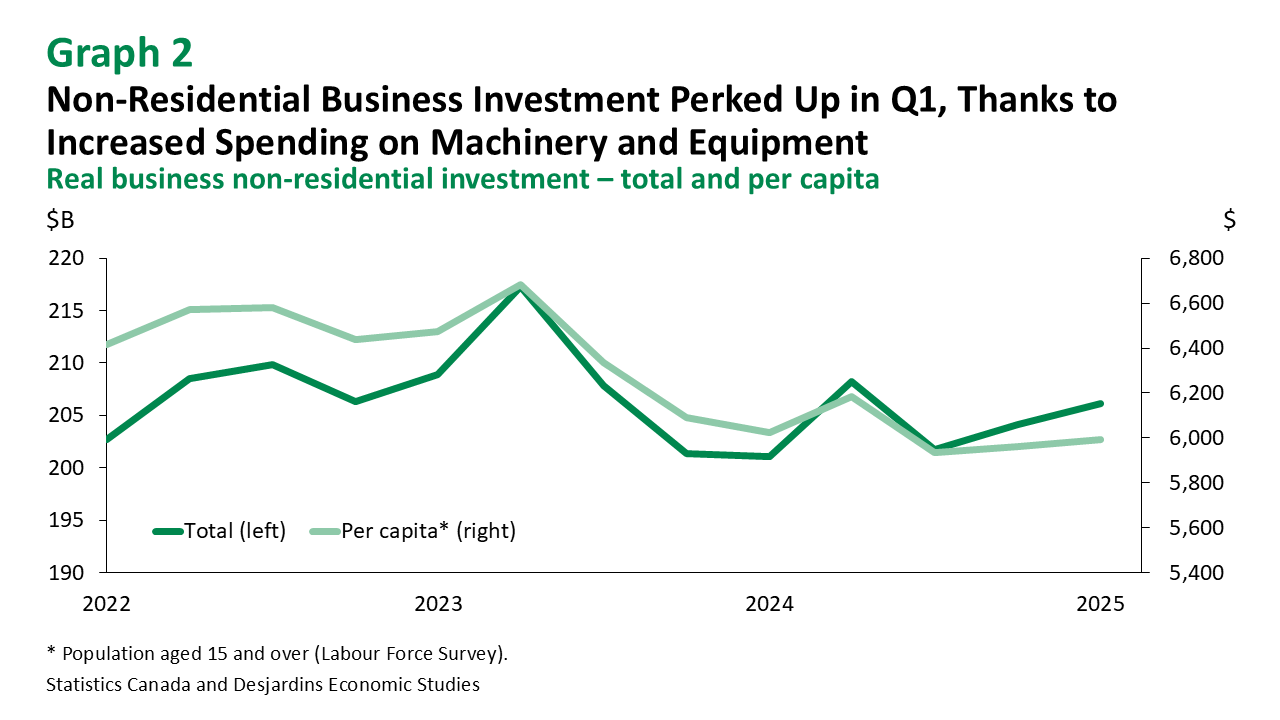

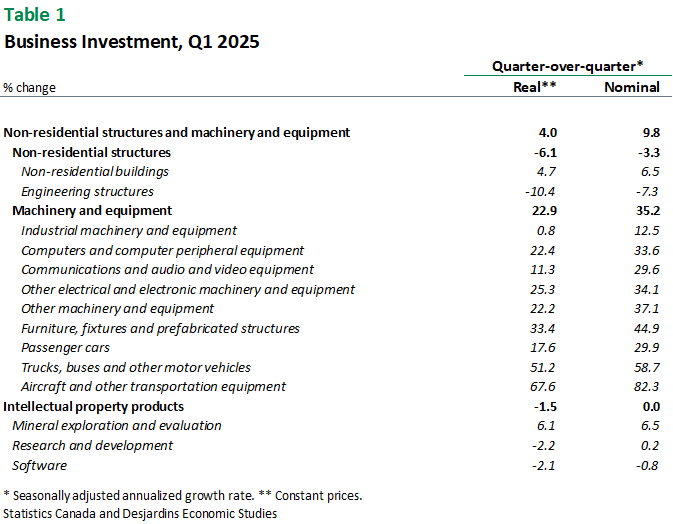

- Despite the uncertain economic environment, non-residential business investment advanced for a second consecutive quarter, with real investments up 4.0% q/q annualized (graph 2). Investments in machinery and equipment (M&E) perked up (22.9%), with all categories posting gains and aircrafts and parts leading the way. This resilience could be linked to firms trying to get ahead of retaliatory tariffs; indeed, Canadian machinery and equipment investment is highly reliant on imports from the US (50.9% of M&E investments were dependent on direct and indirect imports from the US in 2021).

- Business sector investments in non-residential buildings, including factories and plants, also rose in Q1 (+4.7% annualized in real terms). However, a decline in investments in engineering structures (notably in the oil and gas sector) as well as decreased spending in intellectual property weighed on overall growth in real business investments (see table 1 for details).

Implications

As with GDP External link., the tariff context is generating some noise when it comes to interpreting business investment and profit data in Q1 2025. In a quarter marked by consecutive tariff threats, pauses and exemptions, businesses seemed to have braced for a possible upcoming storm by importing key equipment inputs from the US before counter-tariffs hit and building inventories. In Q1, this anticipatory effect even outweighed the negative business sentiment External link. that suggested a contraction in investments was imminent. In all, a second consecutive positive print in non-residential business investment is a welcome surprise and offers a more solid starting point for what’s coming.

What is less certain is how durable this trend will be, and what impact on profits will be felt in the second and third quarters of this year. Non-financial sector net income is looking less resilient, despite tailwinds from higher energy prices in January. With oil prices heading for a decline this year, corporate income will no longer benefit from that helpful boost. And challenges in Ontario’s automotive sector External link. could well bring further hurdles, as uncertainty is already impacting production plans. In all, businesses are facing higher costs and many are reorganizing their supply chains and shifting their export destinations—a process that offers long-term gains but sizeable short-term efforts and expenses. With weaker exports and consumer spending expected to dent revenues, profitability should remain under pressure in a number of sectors in upcoming quarters.