- Randall Bartlett

Deputy Chief Economist

Essentials of Monetary Policy

The First Cut Isn’t Likely to Be the Last

September 17, 2025

According to the Boc

- In line with the widely held view of economists and markets, the Bank of Canada (BoC) cut the overnight policy rate by 25 basis points to 2.50% today.

- In his Press Conference Opening Statement, Bank of Canada Governor Tiff Macklem cited three developments that shifted the balance of risks since the July rate decision. These include a further softening in Canada’s labour market, diminished upward pressures on underlying inflation and the removal of most retaliatory tariffs by Canada.

- On the Canadian labour market, August employment fell for the second consecutive month and the unemployment rate increased to 7.1%. And while the Bank views job losses as being largely concentrated in trade-sensitive sectors, businesses in other sectors of the economy have scaled back hiring intentions. Wage growth has also continued to ease.

- Turning inflation data since the July rate decision, the BoC’s preferred measures of core inflation have been around 3% in recent months. But on a monthly basis, the upward momentum seen earlier this year has dissipated. That said, the BoC believes a broad range of indicators continue to suggest underlying inflation is running around 2.5%.

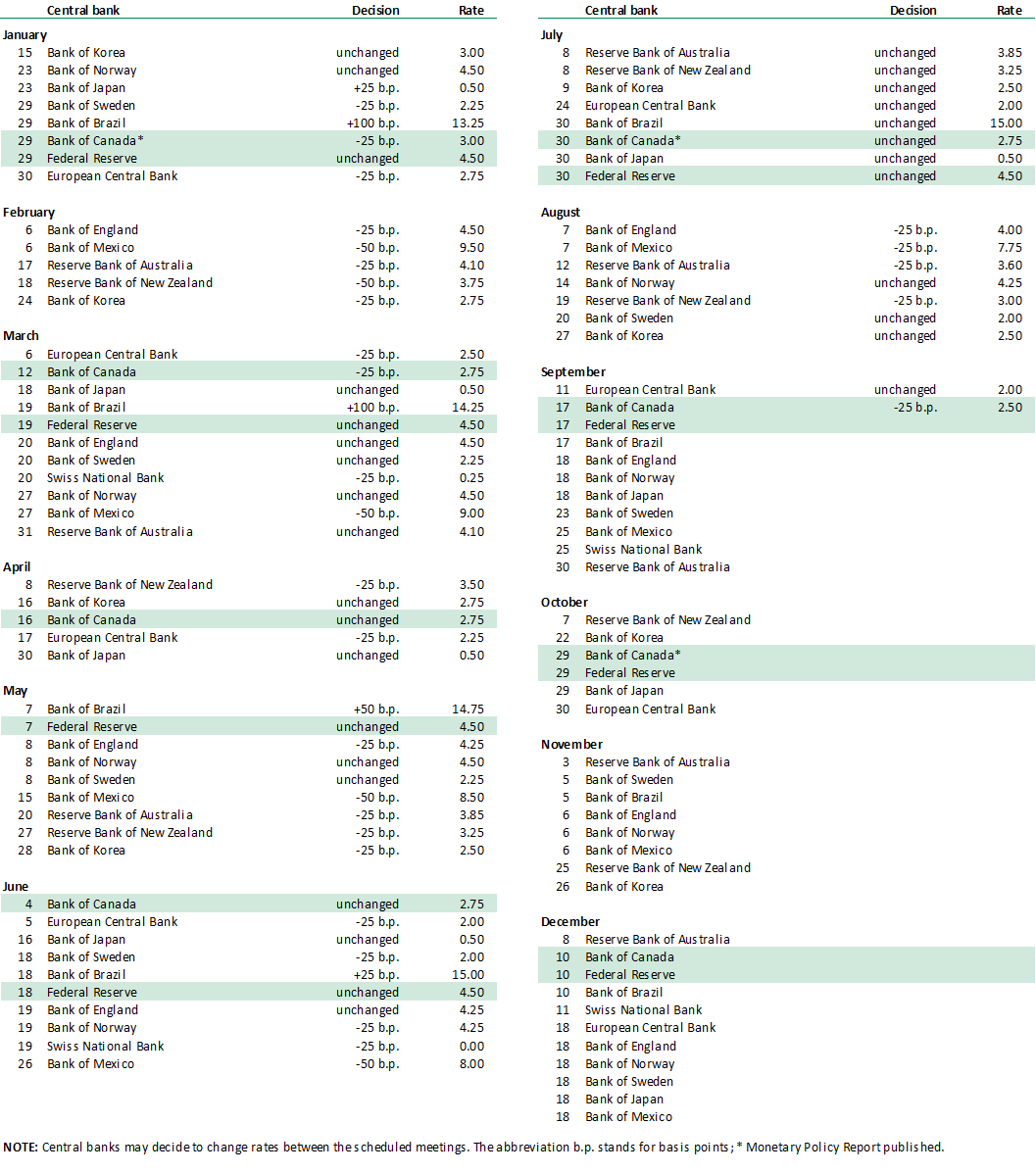

- Last but not least, “the federal government’s recent decision to remove most retaliatory tariffs on imported goods from the United States will mean less upward pressure on the prices of these goods going forward.” By our estimate External link., this could shave about 0.3 percentage points (ppts) from total CPI inflation in 2026 and 0.1 ppts in 2027 (graph 1). That should bring inflation in line with the Bank of Canada’s “de-escalation scenario” from July. That said, Governing Council also made clear that there remains significant uncertainty regarding the inflationary impacts of the ongoing trade dispute.

Implications

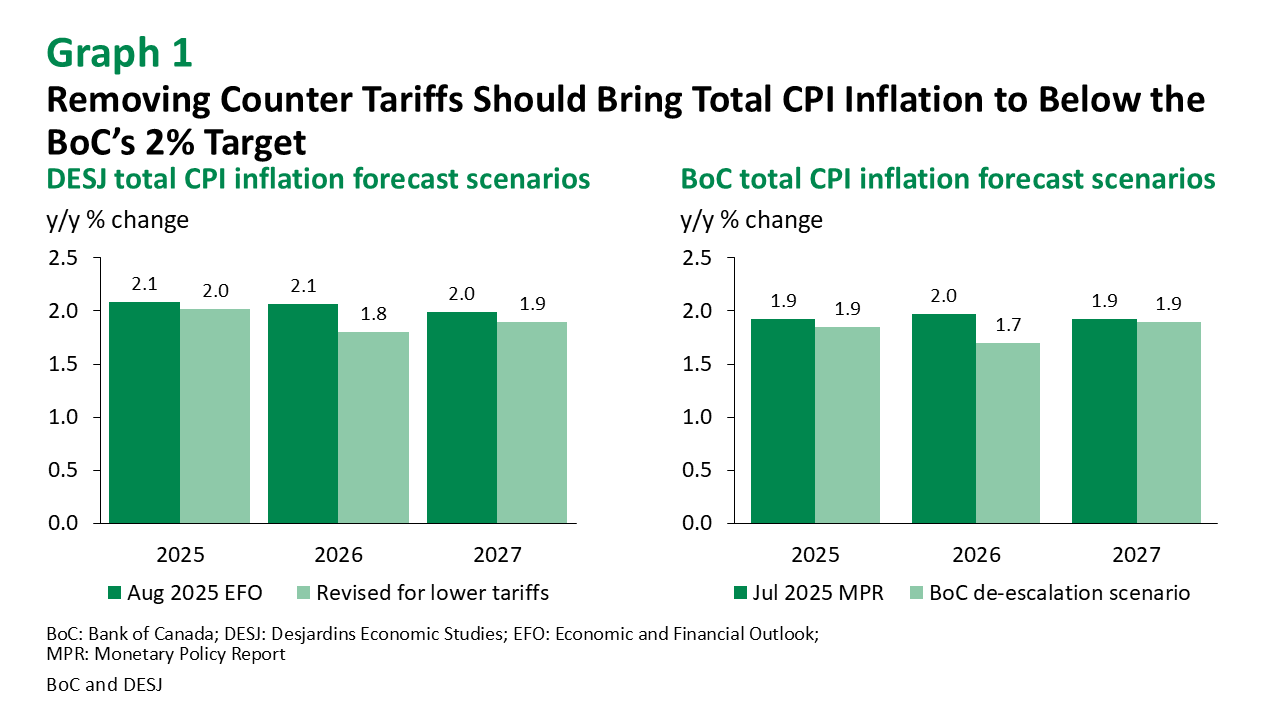

Today’s policy rate cut didn’t come as a surprise to markets and economists. Indeed, we’d been expecting it for some time. The recent labour market External link. weakness and slowing momentum in near-term underlying inflation External link. helped to make the case. The federal government’s reversal on applying counter tariffs on roughly $44B in imports from the US (2024 levels) was the icing on the cake. Not only do we think this will lower the path of inflation in the next couple of years to something closer to the Bank’s de-escalation scenario, but growth is likely to ultimately converge to the level of that scenario as well (graph 2). That said, our real GDP forecast also includes planned federal fiscal policy External link., which was noticeably absent from the Bank’s public statements.

According to the Bank, “there was clear consensus to lower our policy rate for the first time since March.” However, the explicit bias toward cutting that was included in the press release and opening remarks that accompanied the July rate decision have been dropped. In part, this appears to reflect the Bank’s ongoing concern of tariff passthrough into underlying inflation—a risk our research suggests is low. While the Bank worries about supply chain issues resulting from the trade war, it also notes the potential for a weaker job market to stifle domestic demand. The uncertain fate of CUSMA ahead of its review, will likely limit prospects for a near-term investment rebound. As such, we remain of the view that the Bank will cut again in October.

2025 Schedule of Central Bank Meetings