- Tiago Figueiredo, Macro Strategist • LJ Valencia, Economist

Essentials of Monetary Policy

See You in September

July 30, 2025

According to the Boc

- The Bank of Canada held its policy rate at 2.75% for a third consecutive fixed announcement date, in line with the widely held view of economists and markets.

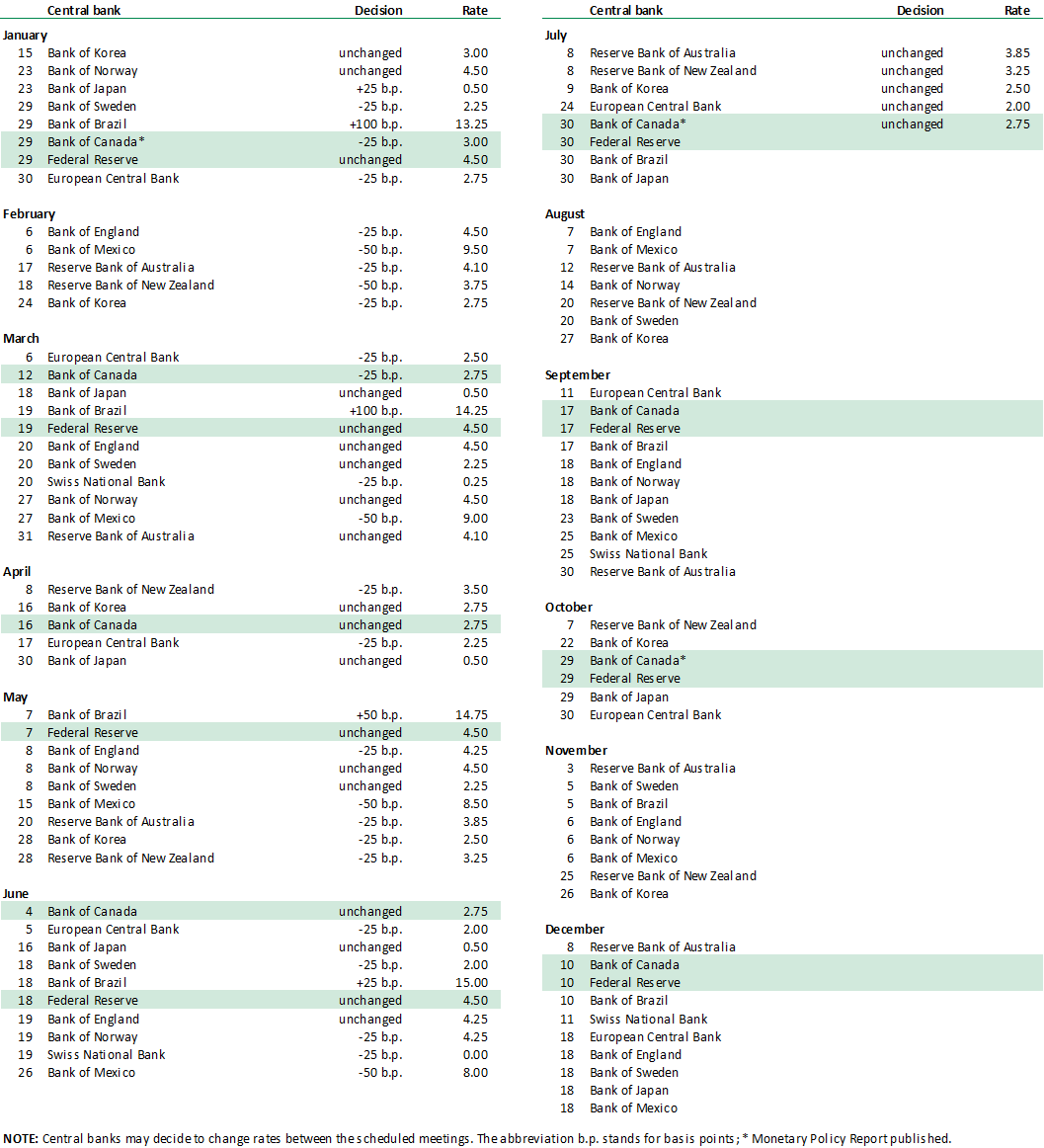

- Policymakers provided three alternative scenarios given trade policy uncertainty (graph 1). While a departure from convention, Macklem clearly stated that this is not impeding the central bank’s ability to make monetary policy decisions. Indeed, there were subtle hints towards a return to rate cuts later this year even if there was a clear consensus to hold the policy rate unchanged today.

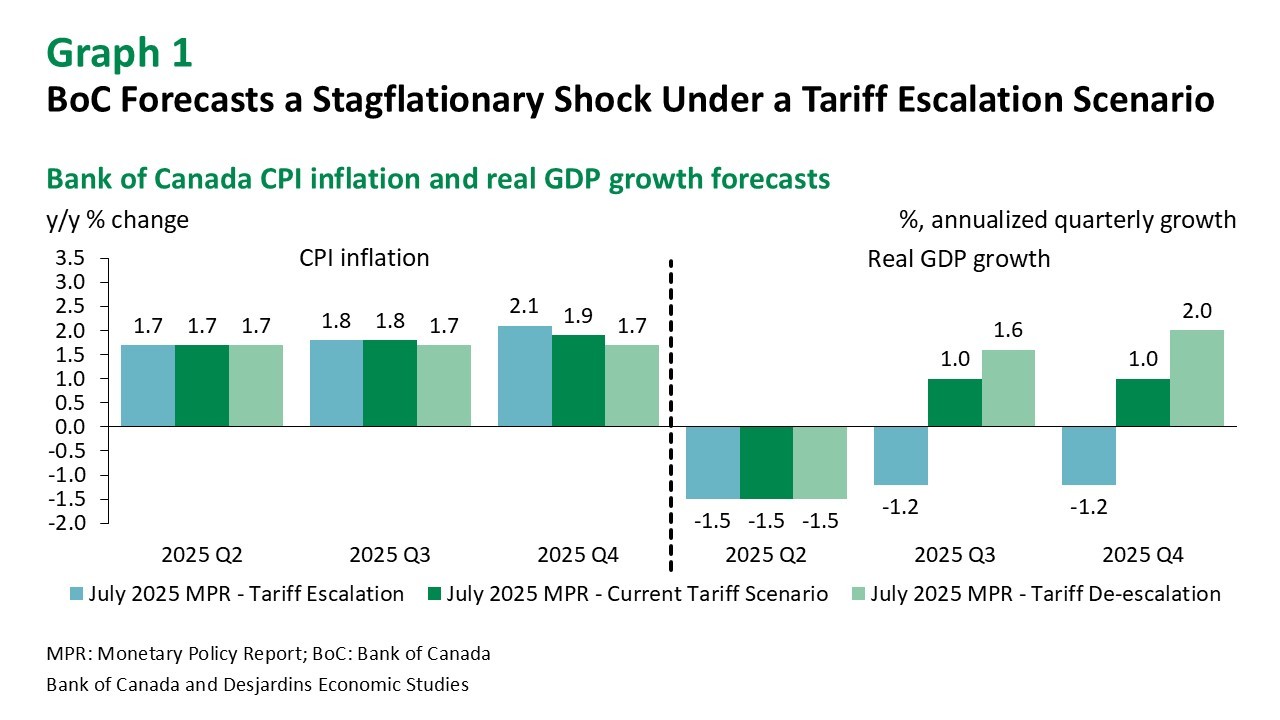

- In the near-term, slack is building in the economy. The Bank of Canada is tracking a -1.5% q/q annualized decline in real GDP growth in Q2 mainly due to a significant drag from net exports with growth stabilizing at a modest 1.0% by the end of the year (graph 2).

- Despite expectations for lower headline inflation, the Bank anticipates inflationary pressures to persist given their higher outlook for core inflation which is expected to rise to 3.1% by the end of 2025.

- Notably, the Bank expects Canada’s counter-tariffs to “add up to 0.6 percentage points to inflation, particularly affecting the prices of goods such as food and motor vehicles”. While that estimate aligns with our earlier estimates, new data suggest it could be on the high side.

Implications

Canadian policy makers are hesitant to cut rates considering lingering concerns about the effects of tariffs on consumer prices and the resilience in the economy. That said, Macklem conceded that there are reasons to believe the recent increase in inflation will unwind gradually. During his press conference, Macklem also struck a more dovish tone when discussing his central bank’s inflation forecasts. Policymakers are aware of the headwinds facing the Canadian economy. In the MPR, officials pointed to mortgage renewals and slowing population growth, even if a portion of these headwinds are offset by incoming fiscal measures. The unemployment rate remains elevated and there was no mention of the strong June LFS reading, suggesting central bankers are taking a more holistic view of the labour market which still indicated slack.

Reading between the lines, it does look like the Bank of Canada is teeing up a return to monetary easing later this year. Two out of the three scenarios presented today lean in favour of further cuts. Furthermore, the inflation forecasts in the current tariff scenario appear to be elevated, particularly considering recent figures on tariff revenues collected by the Canadian government, which have been lower than expected. That opens the door for inflation to print below expectations over the coming months, and help central bankers gain the confidence needed to deliver stimulus. As a result, we continue to see the Bank of Canada cutting rates three times this year, with the first 25 basis point cut coming at the next Bank of Canada fixed announcement date in September.

2025 Schedule of Central Bank Meetings