- Kari Norman

Economist

Economic News

Canada: Q2 Equity-Driven Wealth Gains Skewed Toward Affluent Households

September 11, 2025

Highlights

- Canadian households were more prosperous in Q2 2025 as net wealth increased by 1.5% q/q (up $257.7B to $17.9T)—the seventh consecutive quarterly increase. This advance was due to gains in financial assets (+2.7%), and came despite a small loss in real estate value that weighed on non-financial asset growth.

- Household borrowing eased to $31.6B in Q2, the second consecutive quarterly slowdown. Under the hood, mortgage demand dropped to $24.6B while non-mortgage debt—including consumer credit—rose to $7.0B.

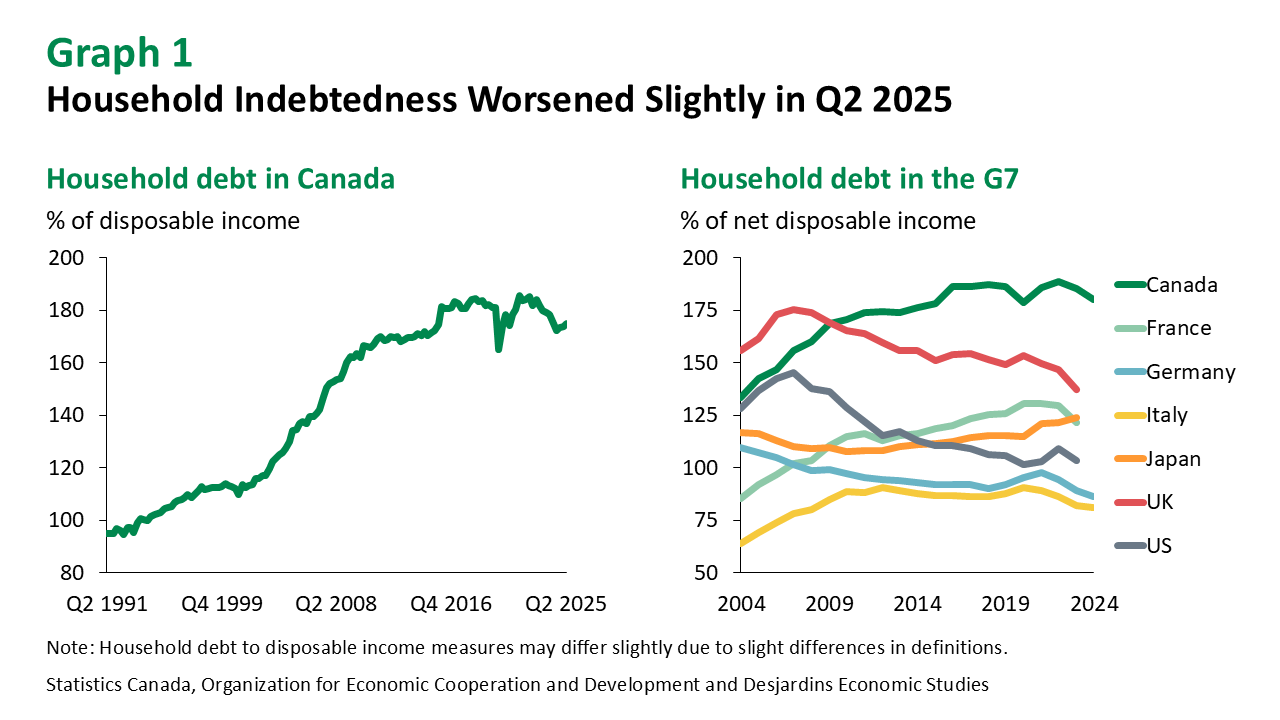

- Household credit market debt tallied $3.1T in Q2. As a proportion of household disposable income, it rose for a third straight quarter, reaching 174.9%, but below the historic high of 185.7% reached in Q4 2021 (graph 1). Canadian households are the most indebted among G7 countries by a wide margin.

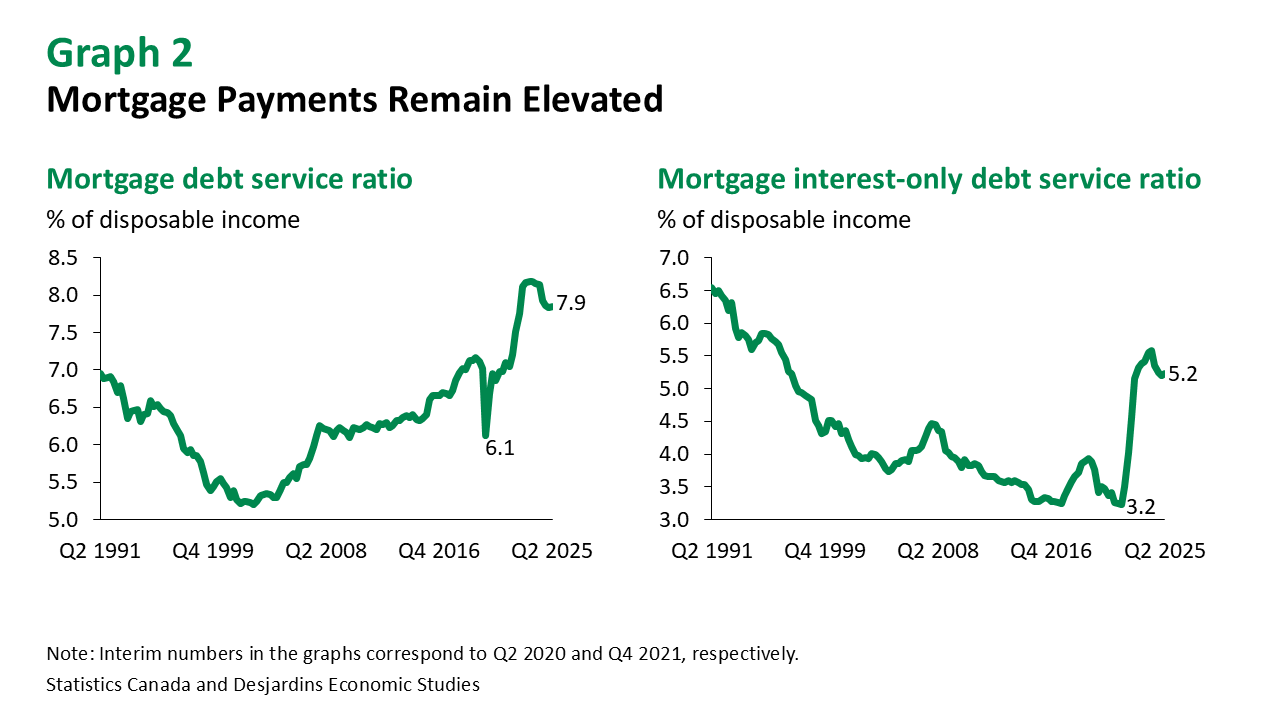

- The household debt service ratio—the share of disposable income directed toward debt payments—rose for the first time in six quarters to 14.4%. This isn’t far from the unprecedented peak of 15.1% reached in Q4 2023. Higher mortgage payments at renewal were likely at play here, as interest payments rose 0.9% while principal payments were little changed in the quarter. The mortgage-only debt service ratio stood at nearly 7.9% in the second quarter, slightly below the record high of 8.2% at the end of 2023 but still elevated (graph 2).

Comments

The Q2 2025 balance sheet release made clear that while Canadian household finances advanced in the quarter, gains were likely not evenly distributed. The wealthiest 20% of households held almost 70% of financial assets and therefore were most likely to benefit from the $291B rise in financial assets. The savings rate External link. continued to slide in the second quarter as the rise in household spending outpaced disposable income gains, falling to 5% from a recent peak of 7.2% reached in Q3 2024. Indeed, consumer spending External link. by Canadian households increased at a solid 5.0% annualized pace in Q2 despite uncertainty due to trade tensions and slower population growth.

Implications

Looking forward to Q3 and beyond, higher monthly mortgage payments at renewal remains a concern to many households, likely holding back consumer spending while encouraging savings in the near term. The labour market External link., while resilient in the face of economic volatility in the first two quarters of the year, has shown weakness of late with summertime back-to-back monthly job losses topping 100k. Wage gains are expected to slow further through the remainder of the year as labour demand weakens, but should continue to outpace inflation. Despite the recent removal of retaliatory tariffs External link. on $44B in US imports, Canada continues to face trade uncertainty as CUSMA nears renewal. Meanwhile, inflation concerns are receding because of this policy shift, clearing the way for the Bank of Canada to resume rate cuts later this month. We maintain our view that the policy rate will need to fall from 2.75% to 2.00% to help stabilize the economy.