- Randall Bartlett

Deputy Chief Economist

Alberta budget

Alberta: 2025–26 Q1 Update

Black Gold Loses Its Luster

August 28, 2025

Comments

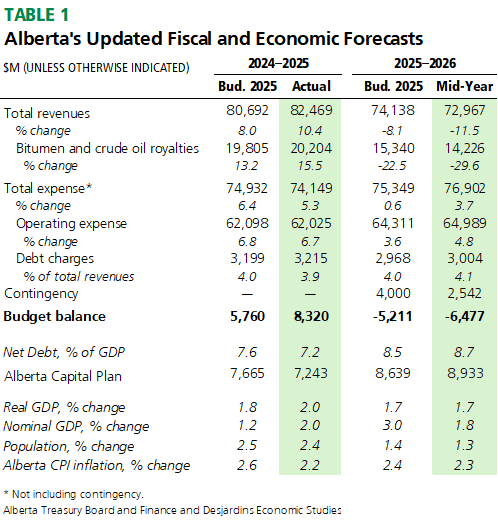

The Government of Alberta released its updated outlook for the 2025–2026 fiscal year (FY2026) earlier today, and the news could have been better. Following a bigger-than-anticipated surplus in FY2025, a $6.5B budget deficit is now expected for this year—$1.3B larger than the $5.2B deficit projected in Budget 2025. See table 1 for details.

Weaker revenues is one explanation for the larger-than-planned deficit in FY2026, now expected to come in $1.2B lower than in Budget 2025 at $73.0B. Non-renewable resources is the driving factor, projected to be $1.4B less in the current fiscal year than back in the spring budget. Tax revenues are tracking below the previous forecast as well (down $349M to $28.5B) but this is more than offset by higher investment income (up $507M to $3.4B).

Expenses also look likely to move higher in FY2026 than projected earlier in the year, up $1.6B to $76.9B. Unforeseen expenditures for disaster and emergency assistance ($706M) are likely to add to higher-than-planned operating expenses (up $679M to $65.0B) and capital grants (up $132M to $3.6B). Debt servicing costs are anticipated to edge higher in FY2026 as well, albeit marginally (up $37M to $3.0B). That should push debt charges as a share of revenues to 4.1% this fiscal year from 4.0% projected in Budget 2025 and 3.9% last year. Drawing $1.5B from the contingency should help offset this higher spending.

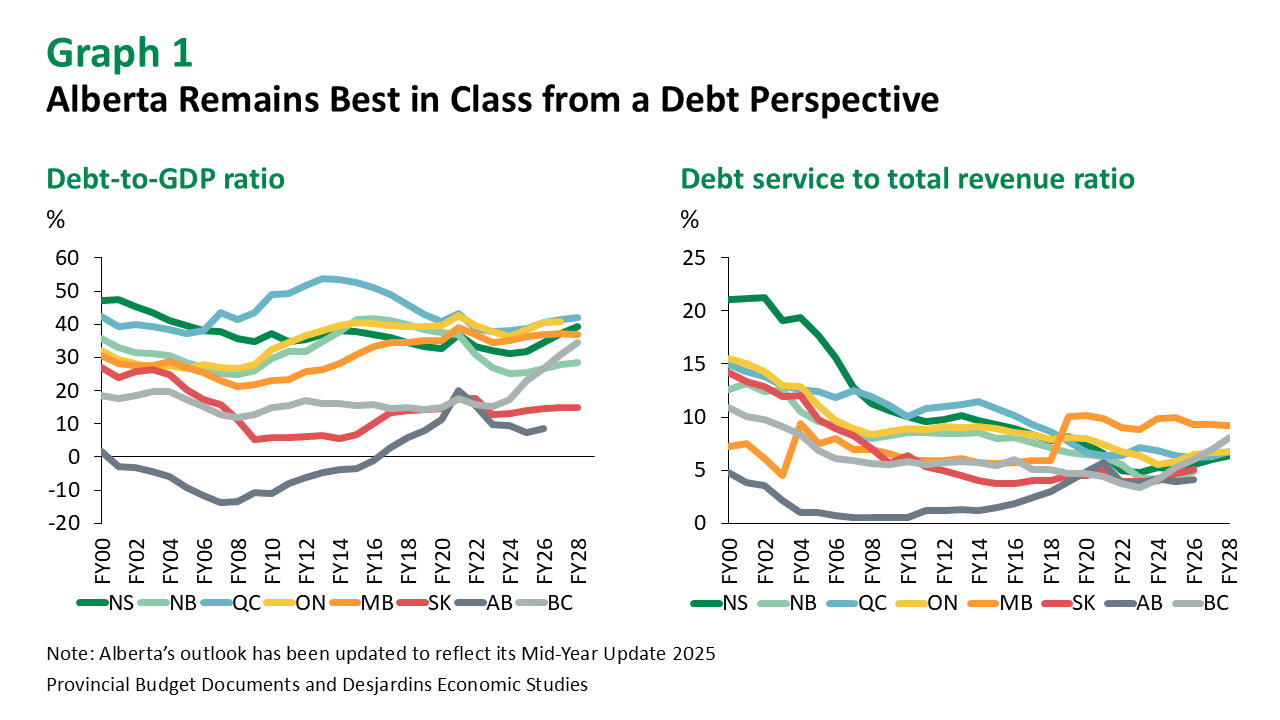

The larger-than-planned budget deficit, combined with the anticipated increase in the total capital plan (up $294M to $8.9B), is expected to push Alberta’s net debt to 8.7% of GDP from 7.2% in FY2025. However, when put in the broader national context, Alberta continues to have the lowest net debt-to-GDP ratio of any province in the country (graph 1), and its borrowing costs reflect that positive performance.

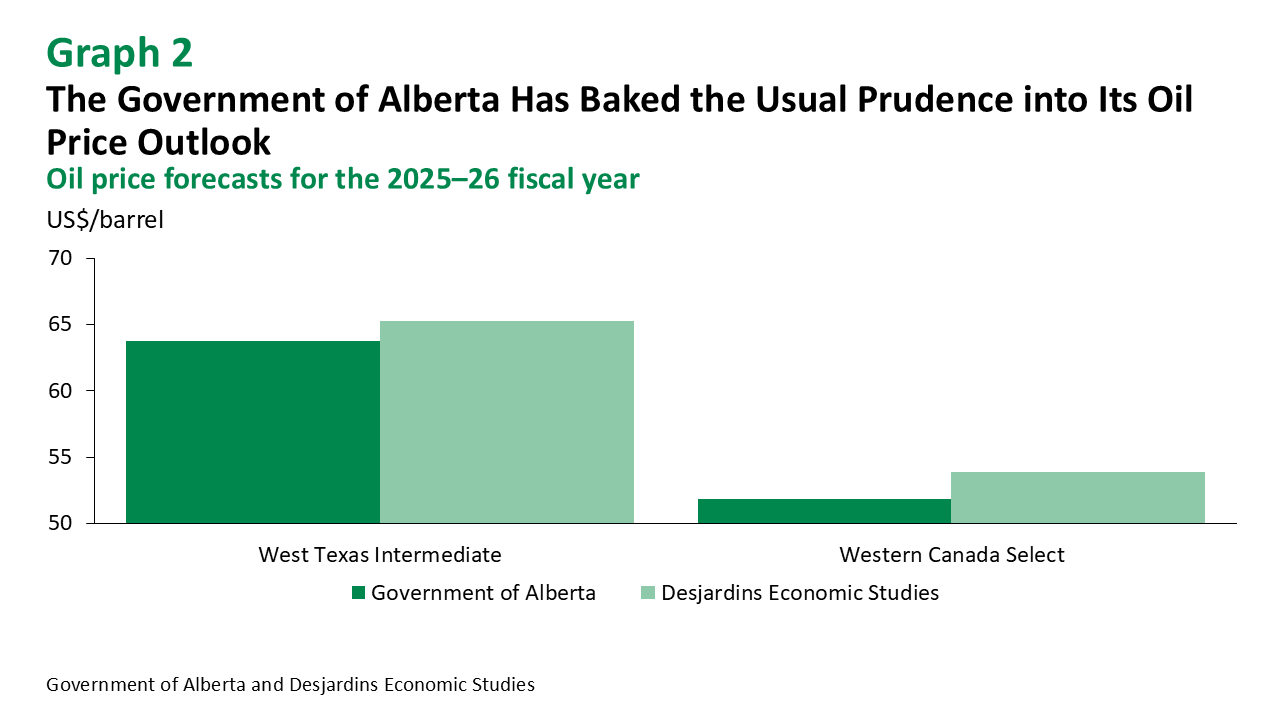

Kicking the tires on Alberta’s latest fiscal outlook, the assumptions for energy prices follow the usual prudence investors have come to expect. At an average price of 63.75 US$/barrel for West Texas Intermediate (WTI), WTI would need to average around 63 US$/barrel for the remainder of the fiscal year to be in line with the Government of Alberta’s planning assumption. At the same time, a light-heavy differential of about 13 US$/barrel for the remainder of the fiscal year is required to average 11.90 US$/barrel in FY2026—wider than any daily spread seen since March. That would put the price outlook of Western Canada Select (WCS)—the Canadian heavy crude benchmark—at about 50 US$/barrel every day through to April 2026. Contrast that with our oil price outlook External link. (graph 2), released earlier today, and it looks as though there may be some upside to the Government of Alberta’s latest fiscal forecast.