It’s time for investors to rethink geographic diversification

A multipolar world implies a review of asset allocation

At the end of the Cold War, the world saw the emergence of what was essentially a unipolar system dominated by the United States—politically, militarily, economically and technologically. Even so, the establishment of the European Union in the 1990s and the rise of China in the 2000s gradually reshaped this balance, while emerging regional powers, such as India, Brazil and Saudi Arabia, also increased their influence. Even though multipolarity had been in the making for some time, the Trump administration’s isolationism and trade war have hastened its arrival, at least from the economic standpoint. This regime shift is clearly not without consequences. A multipolar world is more fragmented and less predictable. It also involves new geopolitical dynamics as some major powers compete for influence while others establish closer relations and step up their trade. A multipolar world can reorganize itself according to changing political and economic interests, contrary to the views apparently held by the Trump administration’s strategic advisers, who act as if American exceptionalism were an immutable truth. Although geographic diversification hasn’t been a key criterion for investors in a unipolar context, the prospect of this new regime makes overexposure to US assets increasingly difficult to justify.

Changes in historical correlations

Since China joined the World Trade Organization in 2001, globalization has intensified, leading to a sharp rise in the correlation of stock market returns between countries. In this context, geographical diversification has proved less useful. The prolonged outperformance of the US stock market since 2010 has also contributed to investors’ lack of interest in international equities. Moreover, institutional investors have favoured a factor-based approach (such as styles, sectors and themes) rather than seeking exposure to a particular country or region. Finally, the growing weight of multinationals, which are, by definition, exposed to the entire world, has also reduced the need for geographical asset allocation.

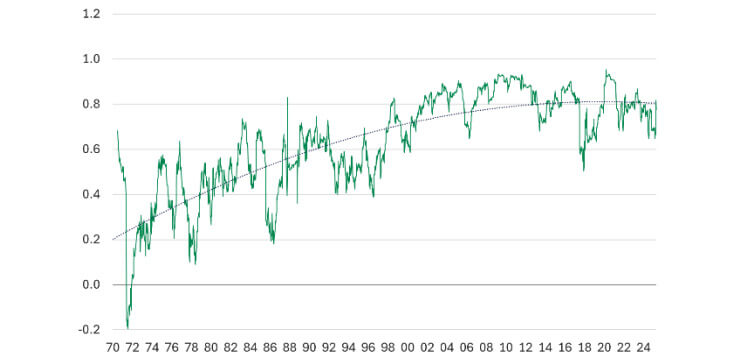

The correlation of returns between stock markets has increased since the 2000s

Correlation between the US and the European equity markets

Weekly returns of the S&P 500 and MSCI Europe

Sources: DGAM, LSEG, April 2025

Description of the Chart of correlation between the US and the European equity markets

This chart shows the correlation between weekly returns of the S&P 500 and MSCI Europe, based on a 52-week moving average from 1970 to 2024.

The vertical scale corresponds to the correlation coefficient (ranging from 0 to 1).

The main line shows the evolving correlation between the two indices. A dotted line indicates the overall upward trend.

General trends observed

- The correlation fluctuates over time, with periods of stronger and weaker alignment between the markets.

- An upward trend suggests increasing synchronization between US and European equity markets over the decades.

Regional equity markets correlation with the S&P 500

Correlations of weekly returns, averaged by decade

Sources: DGAM, LSEG, MSCI, April 2025

Description of the Chart of regional equity markets correlation with the S&P 500

This bar chart shows the correlation of weekly returns between regional equity markets and the S&P 500, averaged by decade, from the 1970s to the 2020s.

The vertical scale corresponds to the correlation coefficient (ranging from -0.2 to 1.0).

For each decade, bars represent the correlations of the following regions with the S&P 500:

- Europe

- EAFE

- Asia-Pacific

- Latin America

- EMOA

- Emerging Asia

General trends observed

- Correlations have generally increased over the decades.

- Europe and EAFE show higher and more stable correlations.

- Emerging markets display more variability, with a rising trend in recent decades.

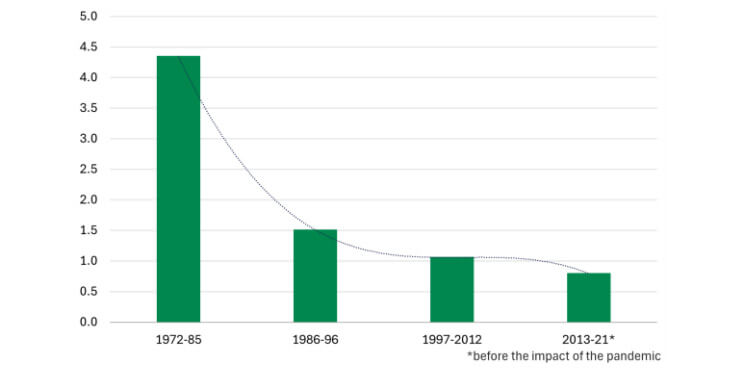

A similar rise in the correlation between bond markets has also occurred since the 2000s. Globalization and the increase in trade flows have significantly reduced the inflation differential between countries. This convergence has helped reduce the dispersion of returns on government debt markets. A multipolar world could lead to higher inflation differentials–even in the short term–as US tariffs and the resulting retaliatory measures unevenly impact supply chains and production costs in different markets.

Lower inflation differentials across countries have increased bond market correlation

Inflation rates dispersion between G7 countries

Standard deviation

Sources: DGAM, LSEG, May 2025

Description of the Chart of the standard deviation of inflation rates

This bar chart shows the evolution of the standard deviation of inflation rates among G7 countries, by time period.

Time periods covered

- 1972–1985

- 1986–1996

- 1997–2012

- 2013–2021 (before pandemic impacts)

The vertical scale corresponds the standard deviation of inflation (from 0 to 4.5).

Each bar represents the standard deviation of inflation for a given period. A dotted line connects the tops of the bars to illustrate the trend.

General trends observed

- Inflation dispersion among G7 countries has steadily decreased over the decades.

- The standard deviation drops from around 4.5 in the 1970s–80s to just above 1 in the 2010s–2021.

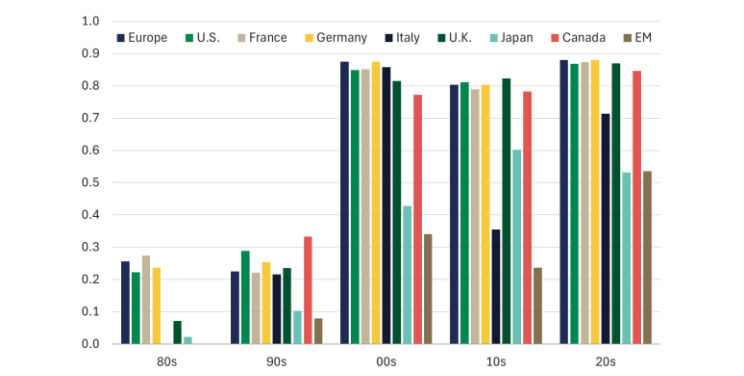

Correlation of bond markets with the world index

Correlation of weekly returns, averages per decade

Sources: DGAM, LSEG, Bloomberg, April 2025

Description of the Chart of Correlation of bond markets with the world index

This bar chart shows the correlation of weekly bond market returns with the world index, averaged by decade, across various countries and regions in the 1980s, 1990s, 2000s, 2010s and 2020s.

The vertical scale corresponds to the correlation coefficient (from 0.0 to 1.0).

For each decade, bars represent the correlation of bond markets from the following regions/countries with the world index:

- Europe

- US

- France

- Germany

- Italy

- UK

- Japan

- Canada

- Emerging markets

General trends observed

- Correlations vary across regions and decades.

- A general upward trend is observed for several countries, indicating increasing integration of global bond markets.

The new trade regime disrupts the supply chain

Optimization of the global supply chain is based on the comparative advantages of countries, such as the quality of their infrastructure, and the strategic decisions that companies make to take advantage of them. It leads to higher profit margins for businesses and lower prices for consumers. International competition thus helps contain inflation, promoting low interest rates and economic growth. In the 1980s, Republican President Ronald Reagan defended such competition, deeming it a driver of innovation, in contrast to protectionism.

Under the Trump administration’s tariff regime, the supply chain of US companies is no longer optimized on the basis of production costs but according to the origin of components. Companies must absorb the inherent cost increase within their profit margins or try to pass some of the increase on to consumers in the form of inflation. Large importers, such as retailers and the automotive industry, are among the most affected. In international markets, US multinationals are also being hit with tariffs in response to their government’s actions.

In contrast, European and Asian multinationals are benefitting not only from a less disrupted supply chain but also from US companies’ loss of competitiveness on international markets and sometimes even from boycotts of their products, Boeing and Tesla being prime examples. That being said, they have to offset their loss of market share in the United States by developing new outlets. New trade agreements between countries deemed to be reliable partners will be the order of the day, at the expense of US firms struggling with their government’s isolationism. The recent free-trade agreement between India and the United Kingdom, as well as the acceleration of trade talks between China, Japan and South Korea, is evidence of the ongoing reorganization.

Obviously, Asian and European firms are not exempt from difficulties under this regime. Those that choose to play the Trump administration’s game in order to maintain market share in the United States have to invest in marginally profitable, or even unprofitable, operations on US soil and absorb part of the tariffs within their profit margins. Even if growth is elsewhere, the United States is still a key market, especially for car manufacturers.

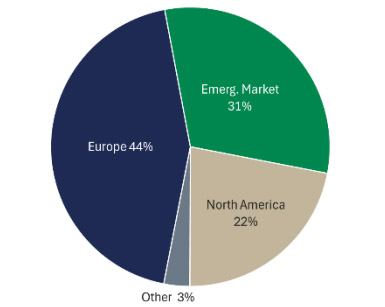

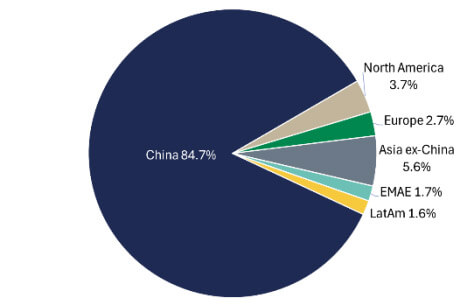

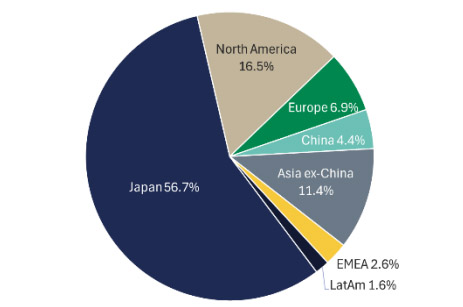

The share of revenues from the United States is low for Chinese companies but much larger for European and Japanese companies

Regional revenue split – Europe

Listed companies

Regional revenue split – China

Listed companies

Regional revenue split – Japan

Listed companies

Source: Morgan Stanley Research, 2024

Description of the Charts of Regional Revenue Split – Europe, China and Japan

This chart shows the geographic distribution of revenue sources for publicly listed companies in Europe, China, and Japan.

There are 3 pie charts.

The first pie chart shows the regional revenue split of listed companies in Europe:

- Europe: 44%

- North America: 22%

- Emerging markets: 31%

- Other: 3%

The second pie chart shows the regional revenue split of listed companies in China:

- China: 84.7%

- North America: 3.7%

- Europe: 2.7%

- Asia ex-China: 5.6%

- EMEA: 1.7%

- Latin America: 1.6%

The third pie chart shows the regional revenue split of listed companies in Japan:

- Japan: 56.7%

- North America: 16.5%

- Europe: 6.9%

- Asia ex-China: 11.4%

- EMEA: 2.6%

- Latin America: 1.6%

General trends observed

- Chinese companies derive the vast majority of their revenue from the domestic market.

- European and Japanese companies show more geographic diversification, with notable revenue shares from North America and emerging markets.

Uncertainty: another burden for US companies

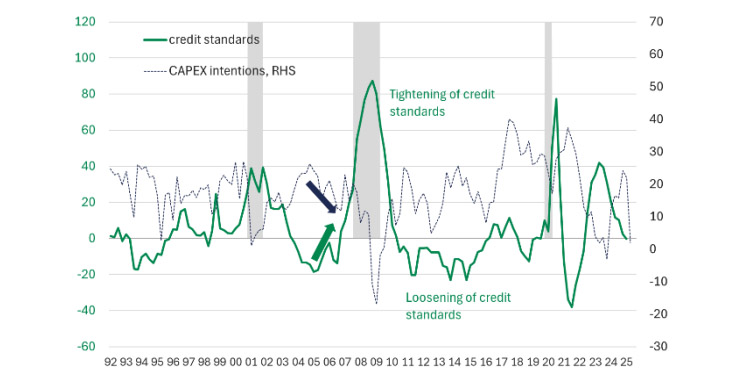

Even though comparative advantages determine a country’s place on the global economic stage, ideological decisions by heads of state can undermine it by holding back a nation’s investment, research and development, and progress. The unpredictability of the economic policies we’re seeing this year is inimical to business investment. In such an environment, long-term investment decisions that require significant capital are likely to be postponed or cancelled. If a company thinks the current administration—or the next one—will reduce or cancel the tariffs, it will shelve its plans to expand, under duress, in the United States. The propensity of banks to lend could also be an issue. If they tighten their credit standards owing to uncertainty, investment will be even more limited. The drastic drop in US business investment intentions this year illustrates the negative impact of uncertainty on capital spending.

An unpredictable environment is unfavourable to investment

Economic policy uncertainty index

United States

Sources: DGAM, Economic Policy Uncertainty, May 2025

Description of the Chart of Economic Policy Uncertainty Index

This chart shows the evolution of the economic policy uncertainty index in the United States from 1985 to 2025.

The vertical scale corresponds to the uncertainty index (ranging from 0 to 700).

The green line shows fluctuations in the index over time. Three shaded vertical bands highlight periods of elevated uncertainty.

General trends observed

Notable peaks occur around 1991, 2001, 2008–2009, and between 2023 and 2025.

The chart illustrates rising uncertainty during times of crisis or political transition.

Bank credit standards and corporate investment – US

Bank lending survey and business survey

Sources: DGAM, LSEG, Federal Reserve, Philadelphia Fed, May 2025

Description of the Chart of Credit standards and Corporate Investment – US

This chart shows the evolution of bank credit standards and corporate capital expenditure (CAPEX) intentions in the United States from 1992 to 2025.

Vertical Scale

- Left axis: Credit standards (ranging from -40 to 120)

- Right axis: CAPEX intentions (ranging from -30 to 70)

There are 2 lines.

- The solid green line represents credit standards.

- The dotted blue line represents CAPEX intentions (right-hand scale).

Two annotated arrows highlight periods of "Tightening of credit standards" and "Loosening of credit standards."

General trends observed

- Credit standards and investment intentions fluctuate with economic cycles.

- Tighter credit conditions often coincide with reduced corporate investment plans.

In contrast, China, Japan, South Korea and the Southeast Asian (ASEAN) countries have recently pledged to collaborate more, increase trade and provide a more predictable environment for business.

The relative valuation of the stock markets offers a useful starting point for diversification

For the long-term investor, it seems like a good time to diversify, from the standpoints of relative valuation and market sentiment (investor appetite) alike. The US stock market is extremely expensive relative to its own history and to other stock markets. Until recently, this American exceptionalism was justified by the greater profitability and the technological advancement of US companies. That being said, new import taxes and less competitive production costs in the United States will undermine profitability. As for the United States’ technological lead, it is rapidly diminishing as China advances.

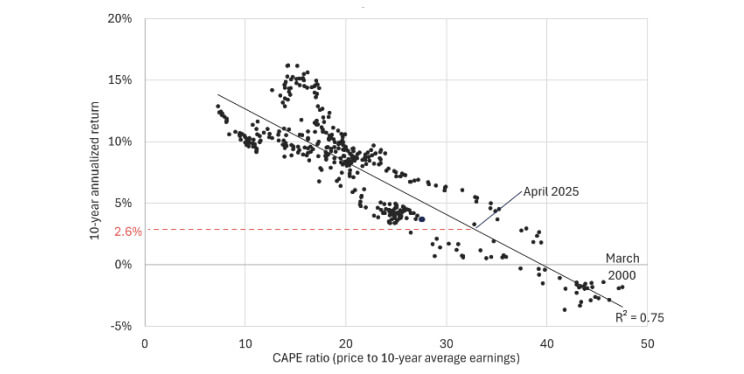

The high valuation of U.S. equities implies their future returns will be less attractive than those of international equities, which are much less expensive

Equity valuation and subsequent return – S&P 500

CAPE ratio (price-to-10-year-earnings) and 10-year subsequent return (1973–2025)

Sources: DGAM, LSEG, May 2025

Description of the Chart of Equity Valuation and Subsequent Return

This scatter plot shows the relationship between the 10-year CAPE ratio and subsequent 10-year annualized returns for the S&P 500.

2 axes

- Horizontal axis: CAPE ratio (from 0 to 50)

- Vertical axis: 10-year annualized return (from -5% to +20%)

Elements Represented

- Each dot represents a historical data point.

- A downward trend line is fitted with an R² of 0.75, indicating a strong negative correlation.

- Notable points include “March 2000” and “April 2025.”

- A red dashed line is drawn at approximately +2.6%.

General trends observed

- Higher CAPE ratios are associated with lower subsequent returns.

- The chart highlights the impact of valuation on long-term investment performance.

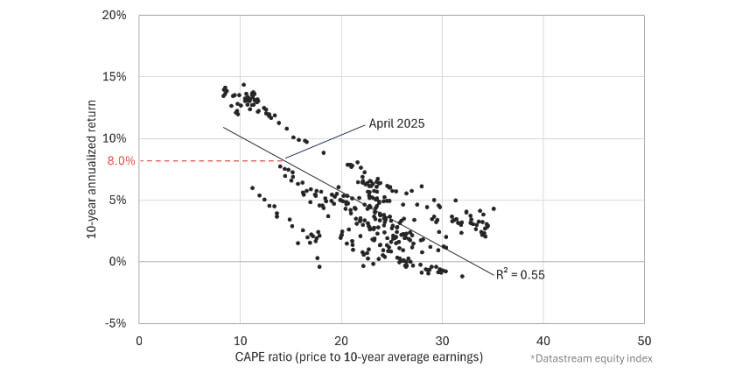

Equity valuation and subsequent return – World ex-US

CAPE ration (price-to-10-year-earnings) and 10-year subsequent return (1973–2025)

Sources: DGAM, LSEG, May 2025

Description of the Chart of Equity Valuation and Subsequent Return – World excluding the US

This scatter plot shows the relationship between the CAPE ratio and subsequent 10-year annualized returns for global markets, excluding the US from 1973 to 2025 (Datastream indices).

2 axes

- Horizontal axis: CAPE ratio (from 0 to over 40)

- Vertical axis: 10-year annualized return (from -5% to +20%)

Elements Represented:

- Each dot represents a historical data point.

- A downward trend line is fitted with an R² of 0.55, indicating a moderate negative correlation.

- “April 2025” is highlighted.

- A red dashed line is drawn at approximately +8%.

General trends observed

- Higher CAPE ratios tend to correspond with lower future returns.

- The chart suggests similar valuation-return dynamics in non-US markets.

Investors’ appetite for US financial assets has been undeniable in recent years, as evidenced by their extremely high allocation to this market, as well as the record concentration of the MSCI ACWI in US equities (more than 64% in 2025 versus 50% in 2014). So, there’s a long way to go in terms of rebalancing and diversification. The unpredictability of the Trump administration, or just its shocking rhetoric, is likely to continue driving capital away. The devaluation of the greenback illustrates the decline in interest in US financial assets since the start of the year. The outperformance of international equities this year could well mark the beginning of a long rebalancing.

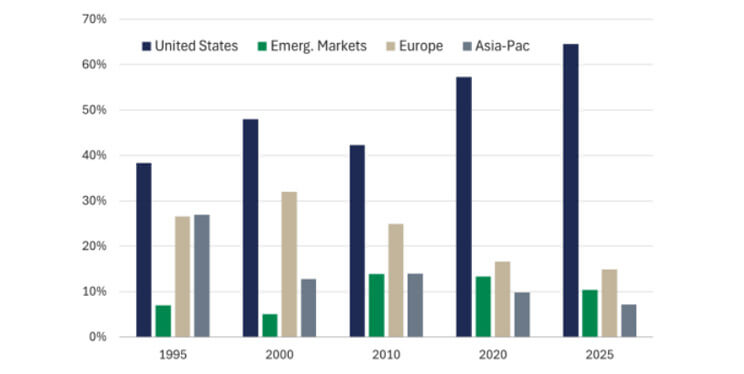

The weight of US equities in the MSCI ACWI has increased significantly over the years

Equity market capitalization

As a percentage of MSCI ACWI (all countries)

Sources: DGAM, LSEG, MSCI, April 2025

Description of the Chart of equity market capitalization

This bar chart compares the equity market capitalization share of four major regions within the MSCI ACWI index across five key years: 1995, 2000, 2010, 2020 and 2025.

The vertical scale corresponds to the percentage of market capitalization (from 0% to 70%).

Bars represented

- United States

- Emerging markets

- Europe

- Asia-Pacific

General trends observed

- The United States consistently holds the highest share of market capitalization.

- Emerging Markets and Europe show similar levels with some variation over time.

- Asia-Pacific maintains the lowest share throughout the observed years.

Conclusion

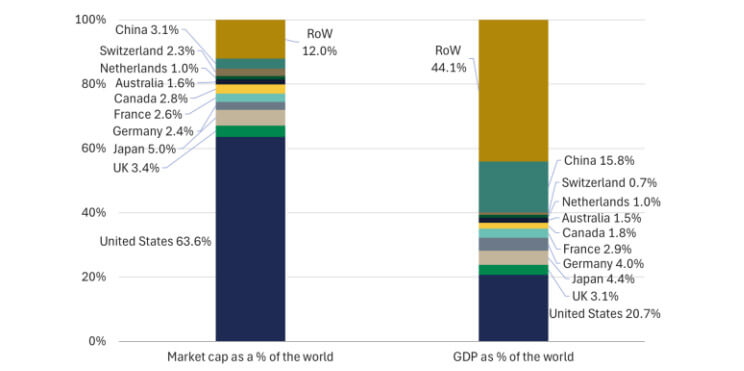

US isolationism is a regime shift that has quickly led to a series of fundamental adjustments around the world, ranging from Germany’s program to modernize its defence and infrastructure to the trade agreements signed in Asia and Europe. All these countries want to quickly reduce their dependence on the United States and diversify their sources of revenue. The United States’ share of the world economy, at about 20%, remains large but is falling. In contrast, the weight of US equities in global market capitalization, at more than 63%, has risen sharply over the years, well beyond what is justified by their fundamentals and growth prospects.

The weight of US equities in the MSCI ACWI has increased significantly over the years

Equity market capitalization

As a percentage of MSCI ACWI (all countries)

Sources: DGAM, LSEG, MSCI, May 2025

Description of the chart of equity market capitalization

This bar chart compares the share of global market capitalization and GDP for various countries.

The vertical scale corresponds to the percentage of global total.

Bars represented

Market Capitalization (% of world)

- United States: 63.6%

- China: 3.1%

- Japan: 5.0%

- Canada: 2.8%

- France: 2.6%

- Germany: 2.4%

- Switzerland: 2.3%

- Australia: 1.6%

- Netherlands: 1.0%

- Rest of the world: 12%

GDP (% of world)

- United States: 20.7%

- China: 15.8%

- Japan: 5.9%

- Germany: 4.4%

- France: 2.4%

- Canada: 1.8%

- Australia: 1.5%

- Netherlands: 1.0%

- Switzerland: 0.7%

- Rest of the world: 44%

General trends observed

- The United States accounts for a significantly larger share of global market capitalization than its share of global GDP.

- China shows the opposite pattern, with a high GDP share but relatively low market capitalization.

- The chart highlights disparities between economic output and financial market representation across countries.

We think a rebalancing is quite likely. The relatively attractive valuation of equity markets outside the US and investors’ limited positioning in them also support rebalancing. Remember that nearly 80% of the world’s economic activity takes place outside the United States. The markets with the fastest-growing middle class, the greatest infrastructure needs and the most abundant labour force are in Asia. The fact that Europe, whose economic weight is equal to that of the United States, is rolling up its sleeves and uniting in response to the many challenges awaiting it could very well contribute to a structural shift that holds promise over the medium and long terms. In a world that is once again multipolar, we’re in favour of rethinking entrenched ideas about sources of diversification and of reviewing investment policies in terms of geographical positioning, the limits of which are often dictated by benchmark stock and bond indexes. To thrive in a changing world, we will have to look boldly beyond the strictures imposed by such benchmarks. To take full advantage of the benefits offered by geographical diversification, don’t hesitate to contact us directly. We offer top-down global equity strategies, with geographical distribution playing a key role in the decision-making process.

Jean-Pierre Couture

Economist and Senior Portfolio Manager

This document was prepared by Desjardins Global Asset Management Inc. (DGAM), for information purposes only. The information included in this document is presented for illustrative and discussion purposes only. The information was obtained from sources that DGAM believes to be reliable, but it is not guaranteed and may be incomplete. The information is current as of the date indicated in this document. DGAM does not assume any obligation whatsoever to update this information or to communicate any new fact concerning the subjects, securities or strategies discussed.

The information presented should not be construed as investment advice, recommendations to buy or sell securities, or recommendations for specific investment strategies. Under no circumstances should this document be considered or used for the purpose of an offer to purchase units in a fund or any other offer of securities in any jurisdiction. Nothing in this document constitutes a declaration that any investment strategy or recommendation contained herein is appropriate for an investor's circumstances. In all cases, investors should conduct their own verification and analysis of this information before taking or refraining to take any action with respect to the securities, strategies and markets that are analyzed in this report.

No investment decisions should be based solely on this document, which is no substitute for due diligence or the required analyses on your part to justify a decision to invest.