- Florence Jean-Jacobs

Principal Economist

Economic News

Business Profits Picked Up in Q3, but Private Investment Is Still Downbeat

November 28, 2025

Highlights

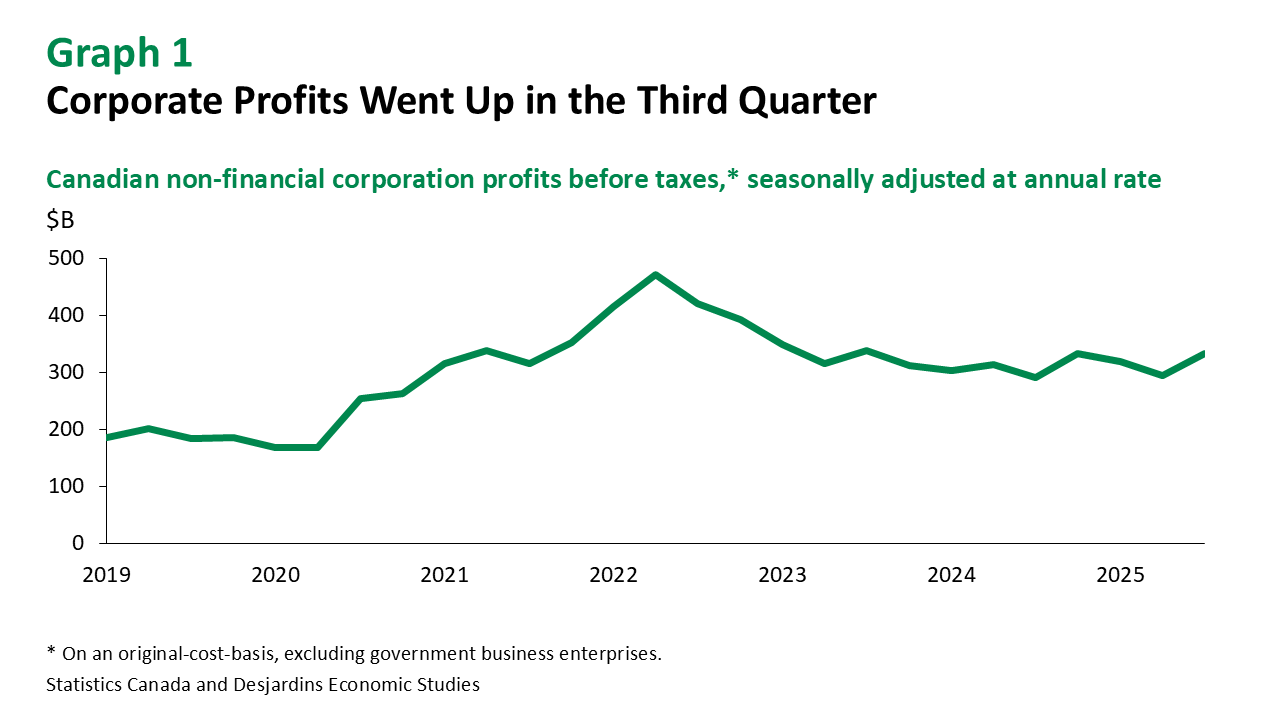

- After deteriorating in the first two quarters of the year, profits of Canadian non‑financial corporations increased in Q3 (graph 1). Both operating profits and net income before tax showed advances (up 7.8% and 25.7% q/q annualized, respectively).

- The improvement in corporate income statements was broad‑based, with 25 of 39 industries posting higher operating profits. This was led by manufacturing and mining, while a contraction in profits in air transportation offset some of the increase, due largely to the flight attendants’ strike in August.

- In the manufacturing sector, higher motor vehicle production and lower operating expenses (some of which was due to temporary shutdowns) helped support profits in Q3, after a tariff‑related decline in Q2. Other transportation manufacturing (aerospace, rail and naval) saw profits climb for a second consecutive quarter.

- The mining industry benefited from higher metal prices, particularly for gold. A rebound in production and exports of crude oil buoyed quarterly profits in the oil and gas extraction sector.

- Higher revenues from a record‑high domestic tourism season boosted operating profits for the arts, entertainment, recreation, accommodation and food services industry.

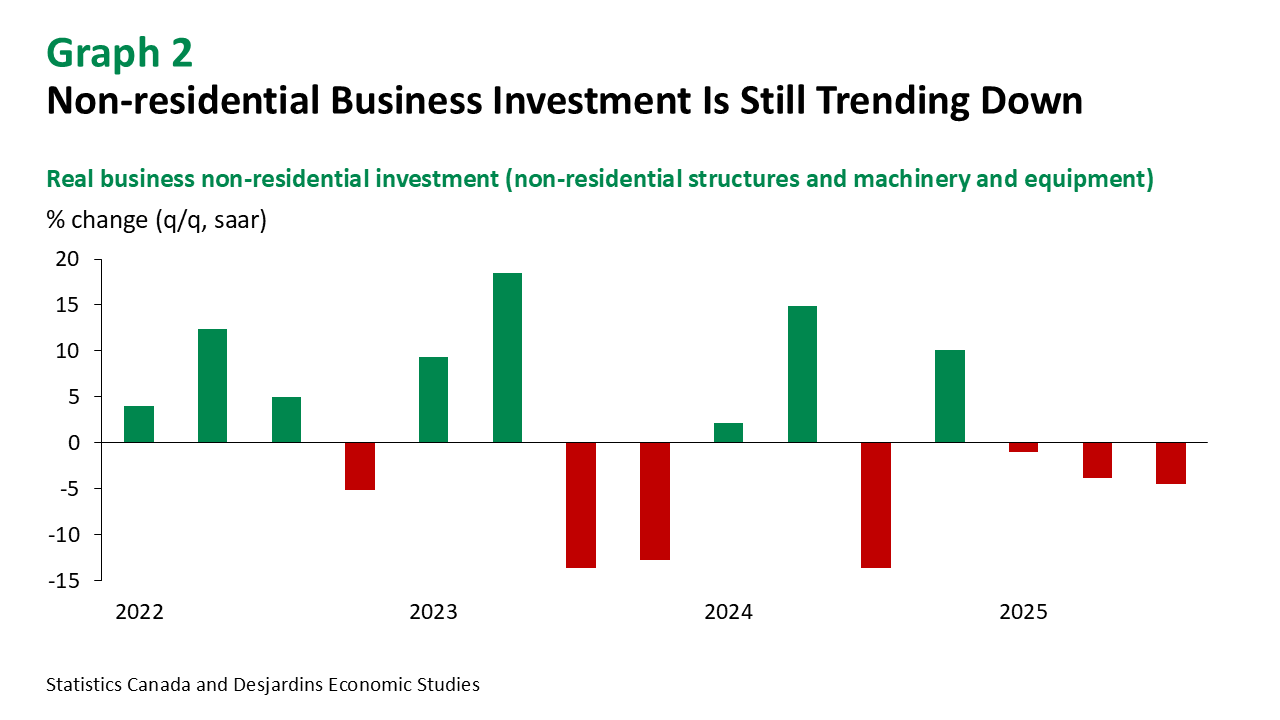

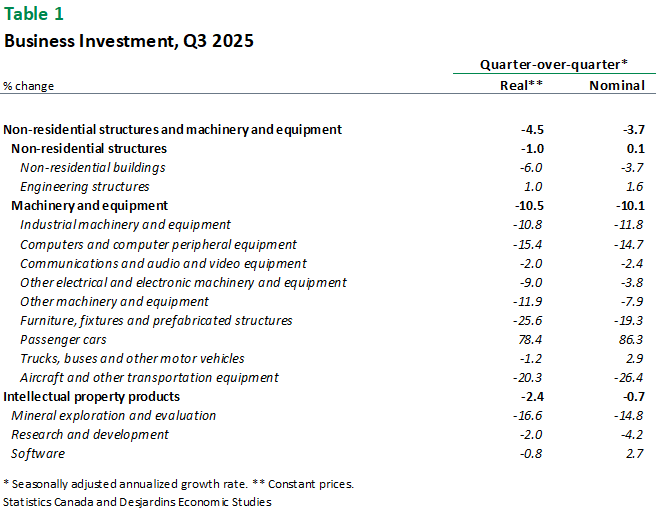

- Improvements in profitability did not translate into higher business investment overall. Real business investment in non‑residential structures and machinery and equipment contracted 4.5% q/q annualized in Q3 (graph 2 and table 1). Only engineering structures saw a quarterly increase (1.0%), while all categories of machinery and equipment posted contractions except for passenger cars. Business expenditures on intellectual property products also contracted, including in R&D (which had otherwise increased in the first half of the year).

Implications

As expected, it appears that low business confidence and an unpredictable trade environment weighed on private sector non‑residential investments in Q3. The quarter was marked by a rise in universal tariffs imposed on non‑CUSMA[1]‑compliant exports from Canada to the US (from 25% to 35%) and 50% US tariffs being applied to a wider array of metal products, as well as new Chinese tariffs of 76% on Canadian canola. There was, however, some relief for businesses importing from the US, with the federal government’s slashing of most retaliatory tariffs External link. as of September 1.

Looking ahead, it will probably take time for business investment to recover from the uncertainty‑induced drag observed from January to September. Indeed, according to the Bank of Canada External link., investment intentions for the next 12 months remained at the same low level in Q3 as in Q2. However, the recently passed federal budget External link. introduced measures that should encourage growth of business capital expenditures, including the so‑called Productivity Super‑Deduction allowing immediate expensing of productivity‑enhancing assets and manufacturing machinery and equipment

The picture of profitability in Q3 confirms that many sectors of the Canadian economy continue to display resilience in spite of disruptive trade policies in the US (as we recently observed External link.). Businesses have clearly taken strides in adapting to the shifting environment. But much will hinge on whether businesses start investing with more confidence in the coming quarters.

[1] CUSMA: Canada-United States-Mexico Agreement.