- LJ Valencia, Economist

Economic News

Canada: Real GDP Saw a Sharp Rebound in Q3

November 28, 2025

Highlights

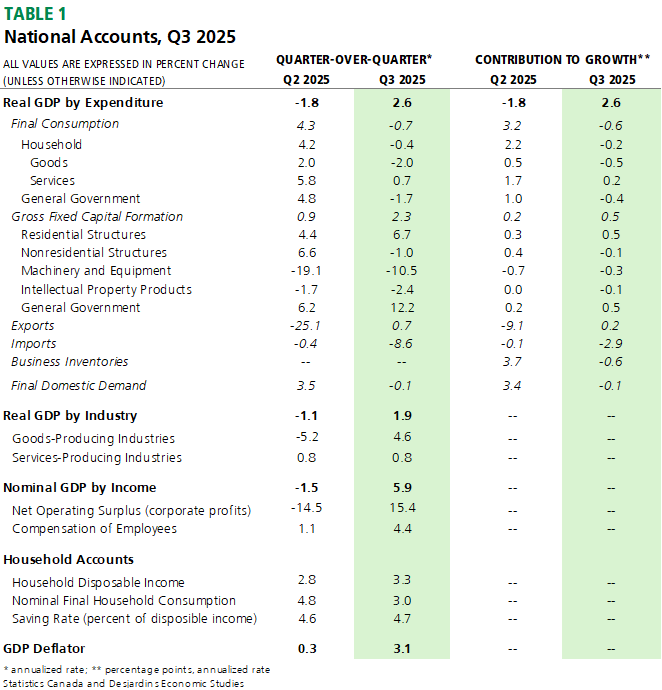

- Real GDP growth increased at an annualized pace of 2.6% in Q3 2025. This was far above the consensus of economic forecasters and the Bank of Canada’s outlook (0.5%). Table 1 provides more details on the release.

- Monthly real GDP rose in September (0.2% m/m), in line with consensus. On a quarterly basis, real GDP by industry advanced by 1.9% q/q annualized in Q3.

- Statistics Canada expects that real GDP by industry fell 0.3% m/m in October 2025, citing decreases in oil and gas extraction, educational services, and manufacturing, being partially offset by increases in mining, quarrying and support services.

Comments

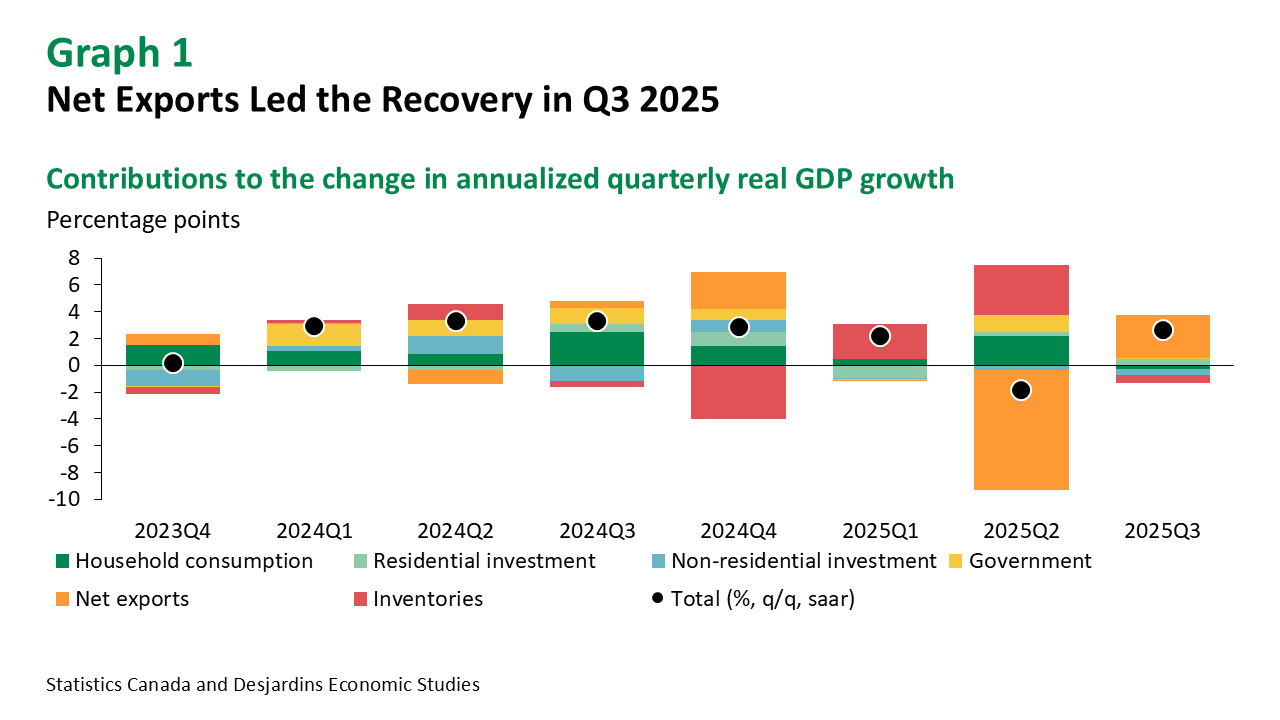

The sharp rebound in real GDP growth in Q3 2025 was led by meaningfully stronger net exports (graph 1). However, the recovery in trade activity was largely linked to a significant drop in imports, which saw its largest decline since 2022 (-8.6% q/q annualized). This fall was caused by a fall in imports of precious metals and industrial machinery, the latter mainly related to the one‑time import of a large oil and gas module in the previous quarter. Exports modestly advanced following a big drop in Q2, up 0.7% annualized, thanks to higher exports of oil products and commercial services.

Real gross investment grew modestly in Q3 (2.3% q/q annualized) on the back of increased government capital spending (12.2%), in large part because of purchases of weapons systems in Canada’s push to meet its NATO targets. Residential investment also rose along with higher ownership transfer costs. In contrast, investment in machinery and equipment fell sharply again this quarter (-10.5%).

In contrast to exports and investment, household spending fell in Q3 (-0.4% q/q annualized) due in large part to lower spending on passenger vehicles. Inventories were also a drag on growth in the quarter.

Compensation of employees saw growth in Q3, up 4.4% annualized. As household income outpacing spending, the savings rate edged up a tick to 4.7%. At the same time, corporate profits grew 15.4% in Q3, largely because of higher output from the oil and gas and mining sectors.

Implications

Overall, while the economy rebounded in Q3, it remains vulnerable amid ongoing trade tensions. Our early tracking suggests that growth in real GDP by expenditure could be around 0.5% annualized in Q4 2025. That’s below the Bank of Canada’s outlook for 1.0% growth published in its October 2025 Monetary Policy Report.

Early signs for Q4 point to a path towards tepid recovery. At the same time, the recently passed federal budget External link. contained spending measures for defence, infrastructure and productivity‑enhancing investments which could provide modest boost to growth in 2026 and beyond. Meanwhile, the recent inflation numbers External link. suggest that underlying inflation may be slightly above the Bank’s 2% target despite the economy remaining in a state of excess slack. As such, we expect the Bank of Canada will keep its policy rate unchanged at the current level at its December rate announcement.