- LJ Valencia, Economist

Economic News

Canada: A New Canadian Immigration Plan

November 5, 2025

Comments

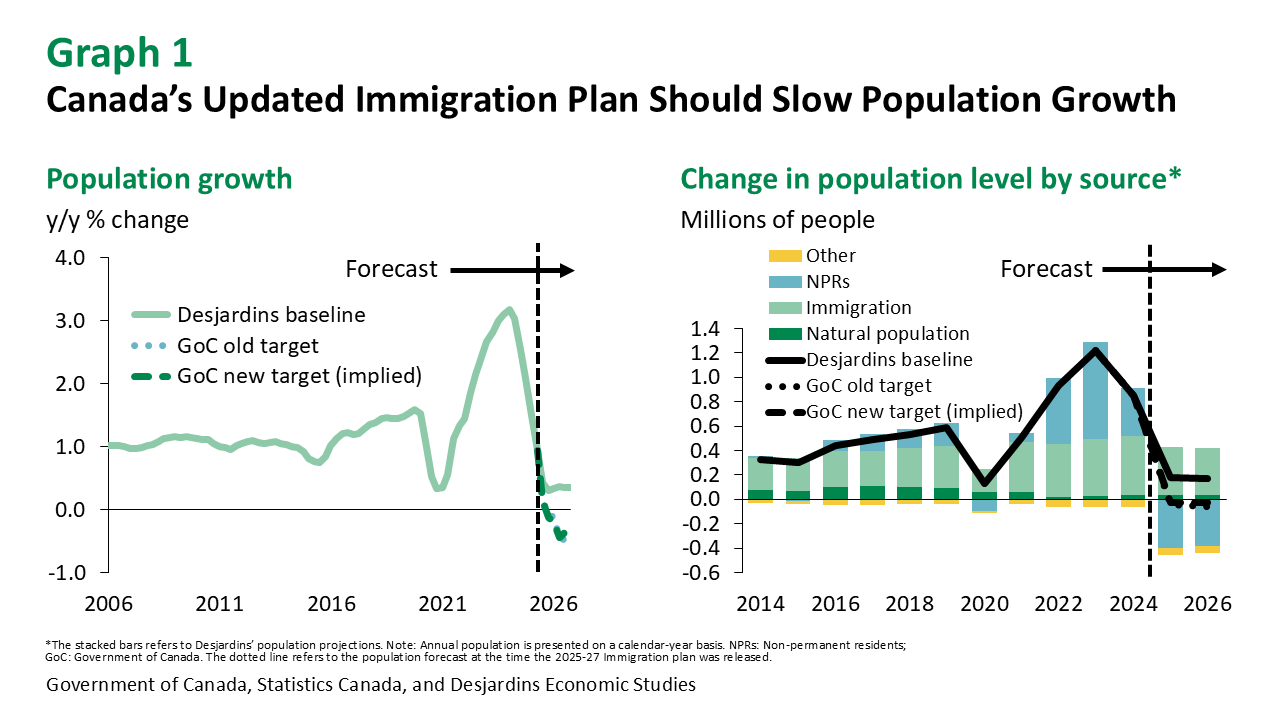

Canada’s immigration strategy appears to be more of the same. In Budget 2025, the federal government announced plans to stabilize permanent resident admissions at 380k over three years, similar to last year’s targets. However, when combined with larger cuts to temporary resident admissions, largely due to lower student admissions, it’s likely population growth will slow further next year as compared to targets announced in 2024 (graph 1).

As the economy undergoes structural changes from the trade war, the new immigration strategy aims to address the unique needs of impacted industries and sectors. Yet, the new plan does little to ease corporate Canada’s concerns about the economic impacts of temporary resident reduction. The plan remains to reduce the level the total number of temporary residents to less than 5% of Canada’s population, but to extend the deadline by one year to the end of 2027. That said, temporary foreign worker targets in the next two years are mostly the same compared to the previous plan.

The new immigration plan offers little relief for cash-strapped post-secondary institutions (PSIs). Under the new strategy, international student admissions are slashed in half compared to the prior plan. PSIs already grappling with declining international student enrollment could face even higher levels of fiscal stress External link. in the coming years.

The goal of this plan is to put immigration back on a sustainable trajectory and alleviate pressures on Canada’s housing market, essential infrastructure and services. That said, Canada has a rapidly aging population, and this revised immigration strategy will compound Canada’s long-term labour force problems and fiscal strains down the line. As shown in previous research External link., there has been a sharp increase in the dependency ratio even under past immigration targets.

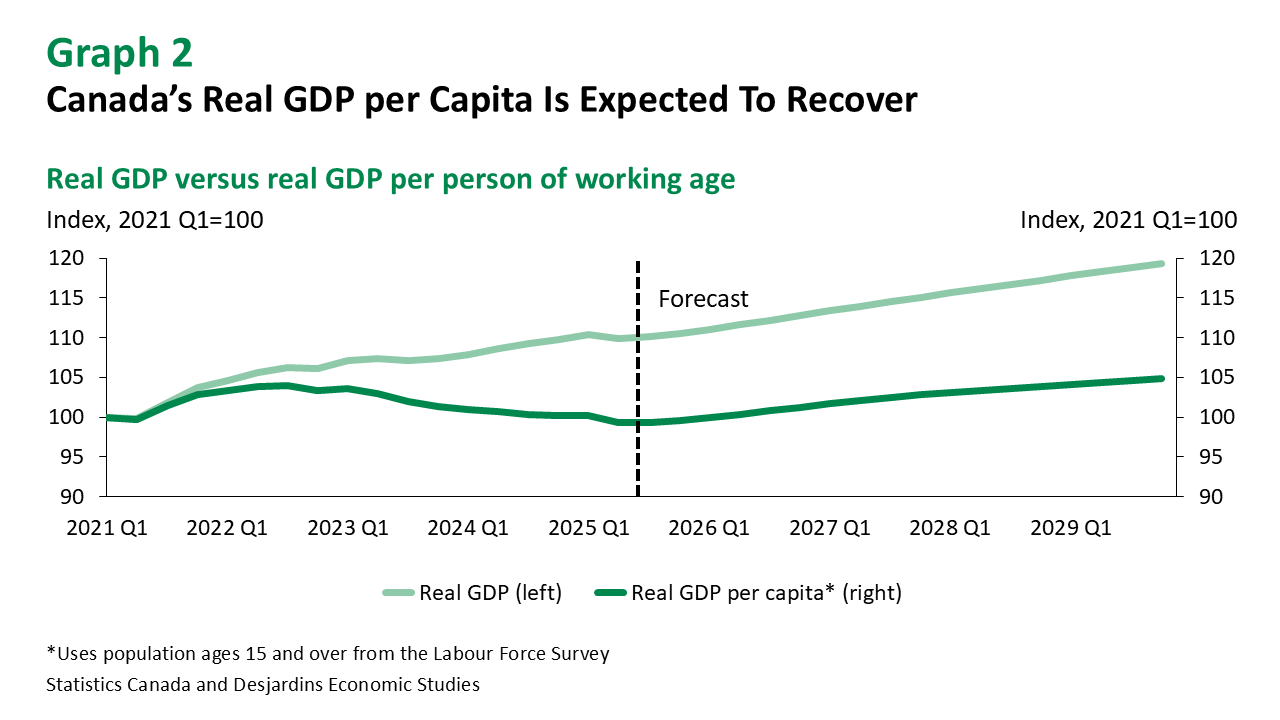

Our population outlook for 2026 is mostly unchanged and the revisions to GDP growth are minimal. The slowing influx of new workers should support wage growth in the near-term, as employers bid to attract fewer available workers. Indeed, the unemployment rate would likely be higher if not for the slower pace of labour force growth. In addition, the slower population growth should ease shelter inflation, particularly in the rental sector, as temporary foreign workers and international students are likelier to rent. Lastly, the slower pace of population growth should help reverse the Canada’s falling GDP per capita (graph 2).

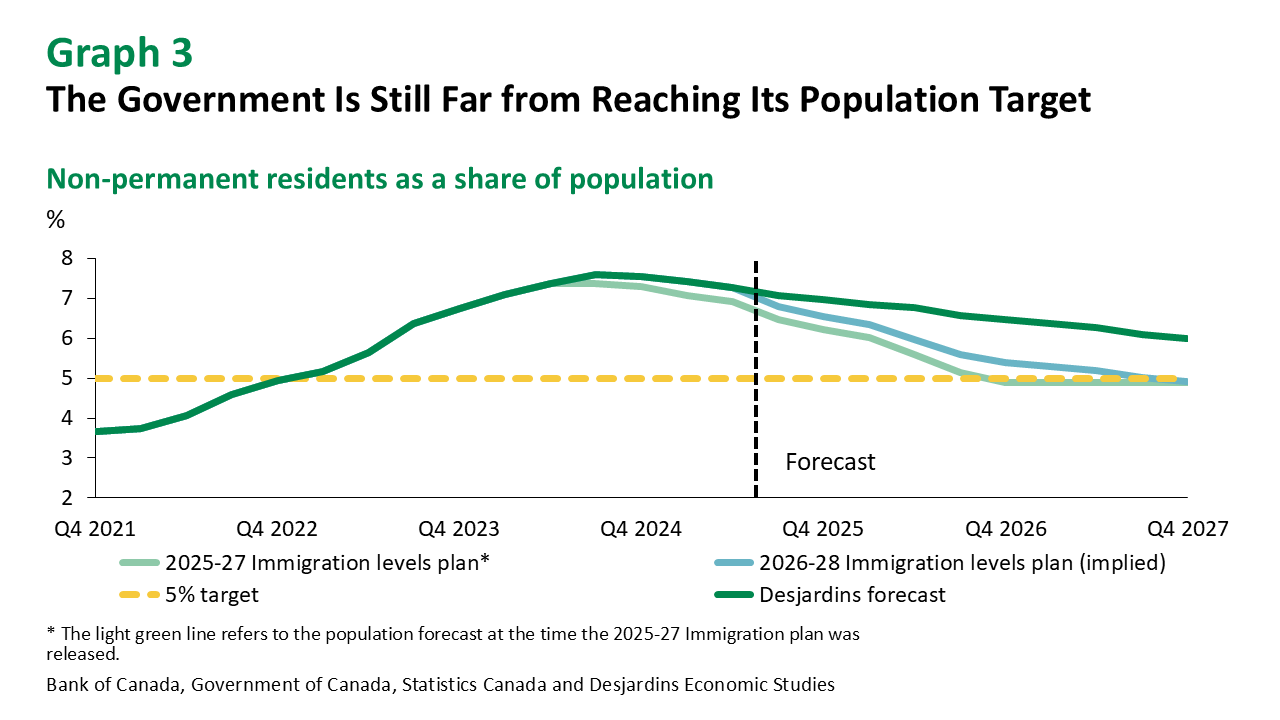

But more work needs to be done if Canada wants to reach its immigration targets. For reasons shown in our past research External link., our outlook remains that the government is unlikely to reach its non-permanent resident target of 5% of total population (graph 3).

The economic impacts from yesterday’s announcements don’t immediately change our outlook for the Bank of Canada. The permanent resident admissions target is mostly unchanged, and the new announcement does little to change our outlook for the output gap in Canada. We anticipate negligible impact on inflation from this announcement and, therefore, the trajectory of the Bank’s policy rates.