- Mirza Shaheryar Baig

Foreign Exchange Strategist

Weekly Commentary

Inflows Up, Loonie Down

November 28, 2025

According to Statistics Canada, foreign investors snapped up C$31 billion in Canadian securities in September—the largest monthly inflow since April 2024. In fact, demand for Canadian securities, especially fixed income, has surged this year. Over the past three months, foreign portfolio inflows to Canadian securities have reached their highest level in more than three years.

Yet the Canadian dollar hasn’t benefited much. How do we square this circle? There are at least three reasons why rising inflows are not translating to a stronger CAD.

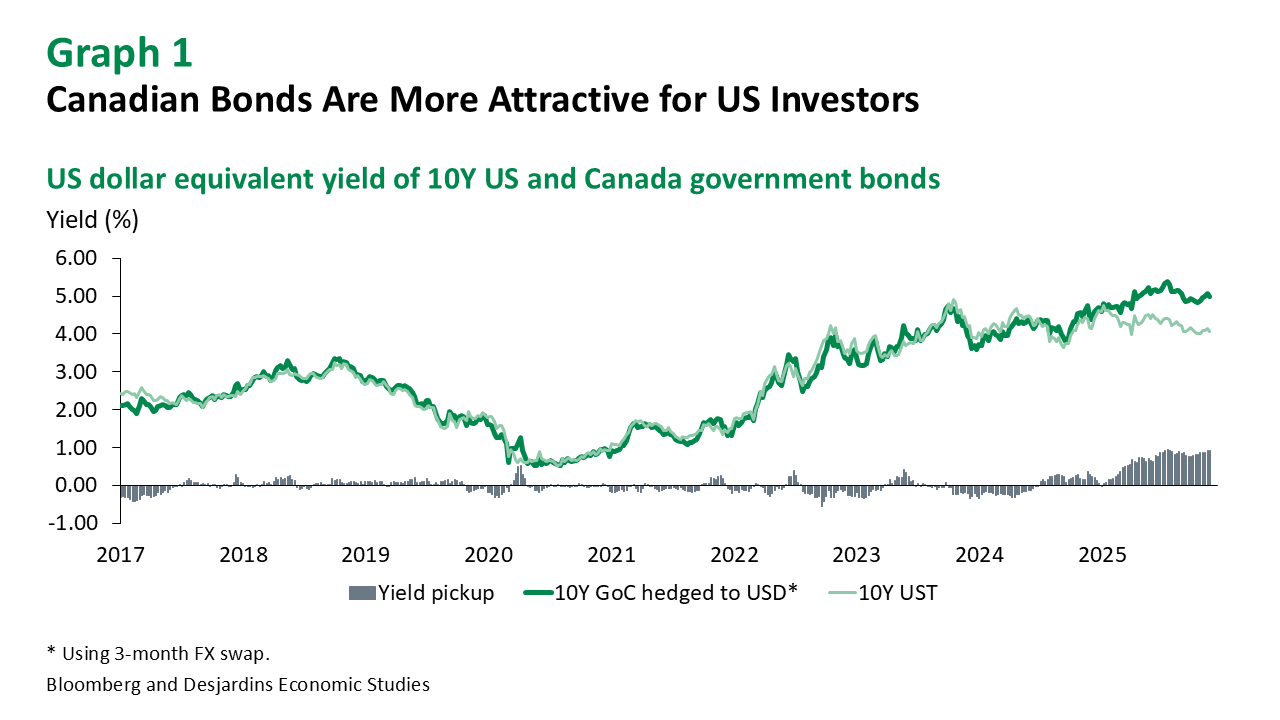

First, most foreign investors are probably hedging their Canadian bond holdings back into US dollars simply because it pays to do so. Short-term interest rates are about 150 basis points lower in Canada than in the US, making it cheaper for US-based investors to borrow in Canadian dollars and then use short-term FX swaps to convert the bonds back into US dollars. As graph 1 shows, US investors can earn about 90 basis points above the yield on 10‑year Treasuries by buying 10‑year GoCs and swapping back into dollars.

Second, about one-third of the money flowing into Canada this year went into securities issued in foreign currencies, not Canadian dollars. Why does that matter? Because when the federal government, provinces or companies like gold miners issue US dollar bonds (“Yankee bonds”), the proceeds usually stay in US dollars or are hedged by the issuer. In other words, very little of that money actually gets converted into Canadian dollars, so the impact on the loonie is minimal.

Third, Canadians have been pouring money into foreign assets, especially US stocks. After a short pause following “Liberation Day,” they ramped up buying again in recent months. Over the past three months, purchases of US equities hit a record C$73 billion in September—the highest ever.

In short, record-breaking inflows haven’t translated into a stronger Canadian dollar because much of that money never truly enters the FX market. Hedging practices, foreign currency issuance and Canadians’ own appetite for US assets have offset the headline numbers. Until these dynamics shift, large portfolio inflows alone won’t be enough to lift the loonie.