- Randall Bartlett, Deputy Chief Economist • LJ Valencia, Economist

Essentials of Monetary Policy

The Bank of Canada Is ‘Two and Through’ for the Current Round of Rate Cuts

October 29, 2025

According to the Bank of Canada (BoC)

- The Bank of Canada cut its policy rate by 25 basis points for the second consecutive meeting to 2.25%, in line with the widely held view of economists and markets. The policy rate is now at the lower bound of the Bank’s estimated range for the neutral rate.

- In his Press Conference Opening Statement, Bank of Canada Governor had four main messages:

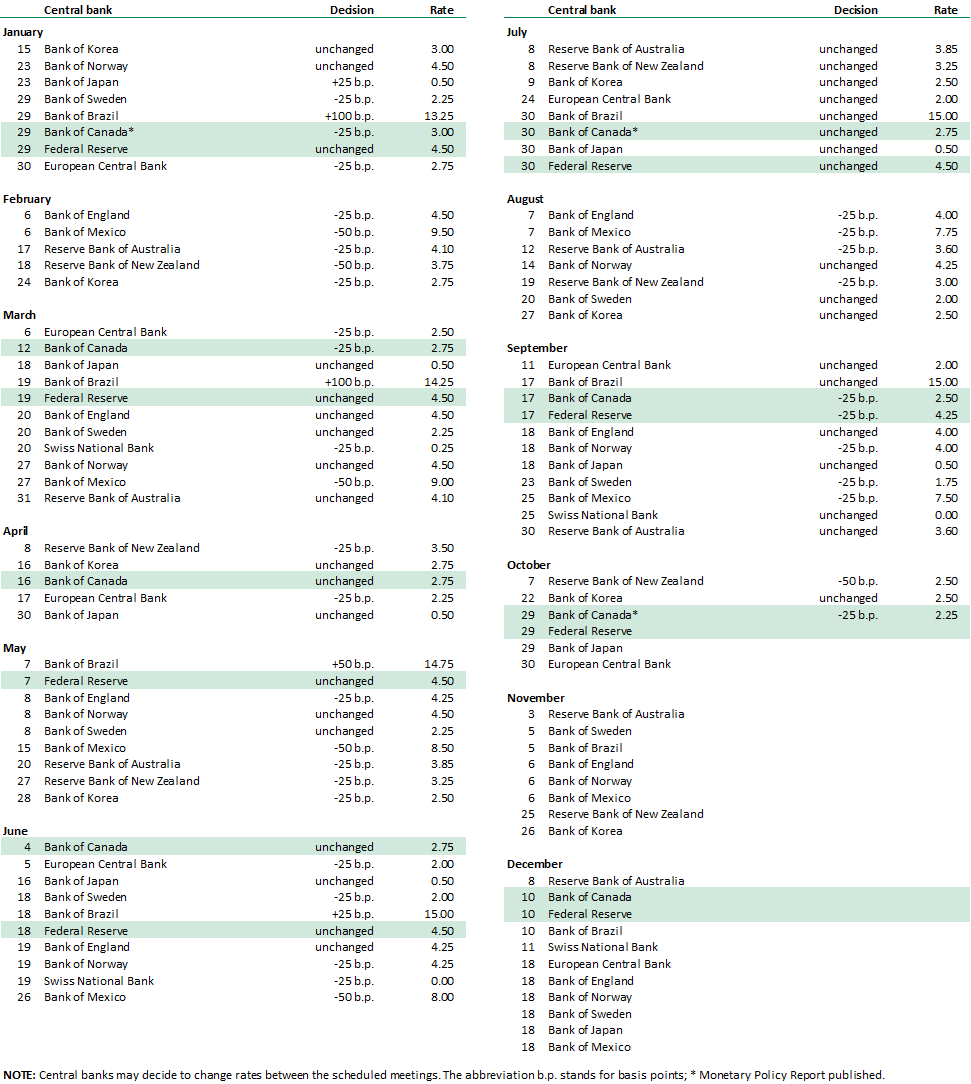

- First, the Canadian economy has been weakened by US tariffs and trade policy uncertainty, and that is expected to weigh on growth through the remainder of the year. The labour market is soft. The Bank’s forecasts for real GDP growth in the second half of the year has been marked down from that in the July 2025 Monetary Policy Report’s (MPR) current tariff scenario (graph 1). The BoC has kept its sluggish outlook for 2026 largely unchanged.

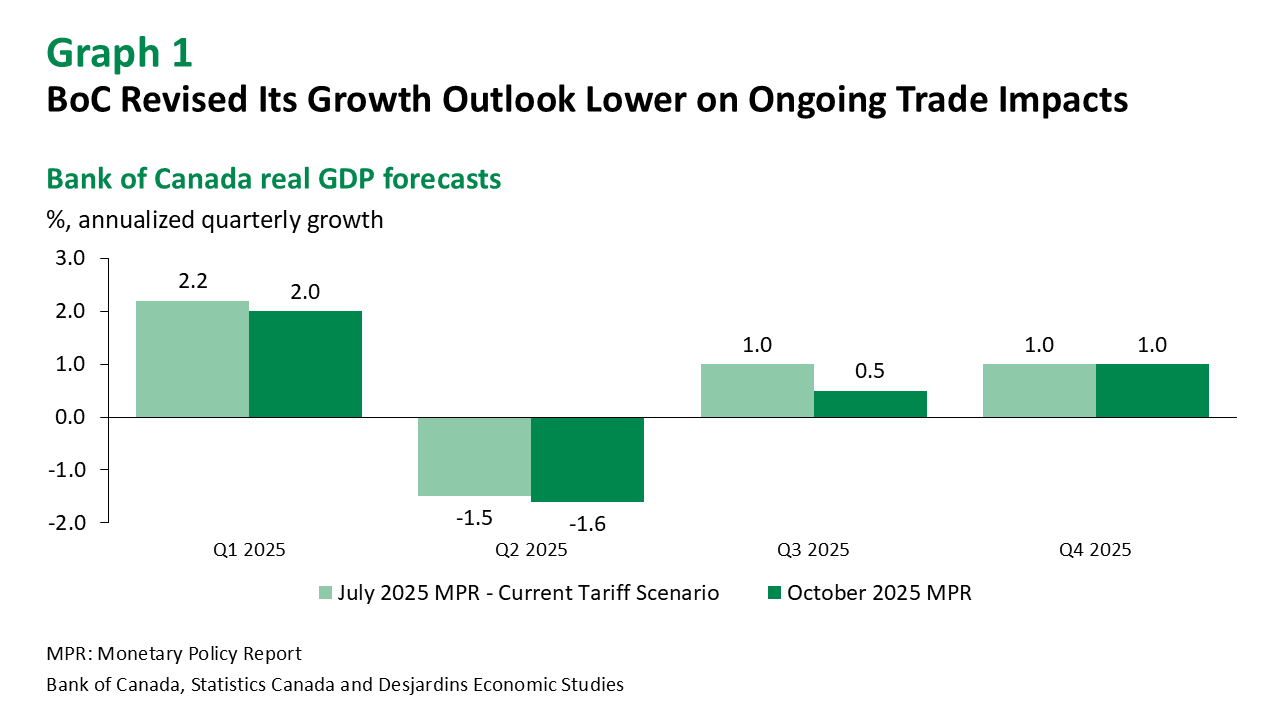

- Second, while economic weakness is holding back price increases, the trade conflict is adding to the costs facing businesses, thereby putting upward pressure on inflation. The BoC expects these factors to broadly be a wash, keeping inflation to around 2% over the outlook. That said, the Bank revised up its outlook for inflation slightly compared to the July MPR (graph 2).

- Third, the Bank has lowered the overnight policy rate by a total of 50 basis points at its last two meetings. Overall, rates have been cut by 100 basis points since the start of the year to support the economy through this period of adjustment.

- Fourth, the weakness in the Canadian economy is more than just a cyclical downturn. It’s a structural adjustment to a lower output path driven by US trade policy, limiting monetary policy’s ability to boost demand while maintaining low, stable and predictable inflation.

Implications

While today’s rate cut by the Bank of Canada was widely expected, the bar is high for further monetary policy support. From the Press Release that accompanied the rate decision, “Governing Council sees the current policy rate at about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment. If the outlook changes, we are prepared to respond.” We are now of the view that the Bank of Canada will keep interest rates on hold for the foreseeable future.

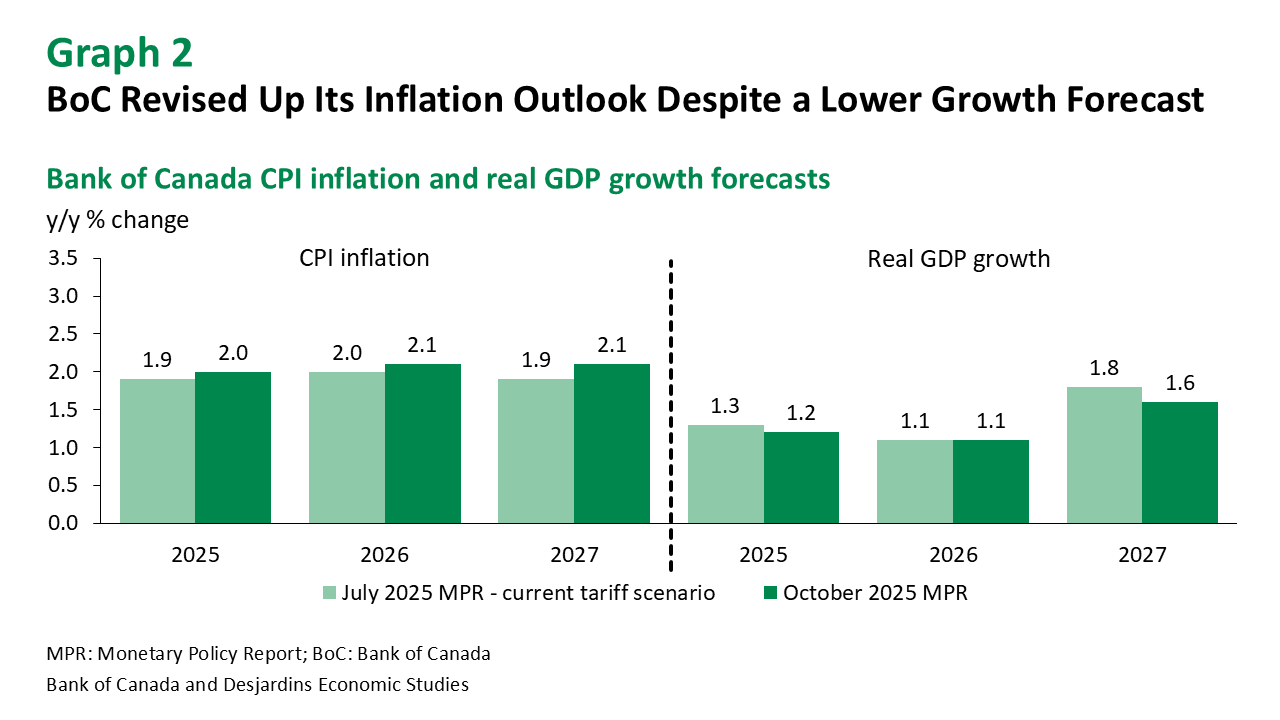

Our baseline outlook External link. for the Canadian economy is more positive than the Bank’s, despite the risks to the outlook remaining tilted to the downside due to the uncertainty of US trade policy (graph 3). First, our analysis External link. suggests that the removal of countertariffs on most previously dutied imports from the United States should boost growth in 2026 by about 0.2 percentage points (ppts). Second, by convention, the BoC has not yet accounted for the substantial expansion in federal fiscal spending that is expected to accompany next week’s 2025 budget (see our preview External link.). This is likely to provide a meaningful tailwind to economic growth starting in mid‑2026, to the tune of roughly 0.3 ppts next year, and should result in an upward revision to the Bank’s forecast in its January 2026 MPR. Notably, our forecast for inflation remains in line with the BoC’s 2% target.

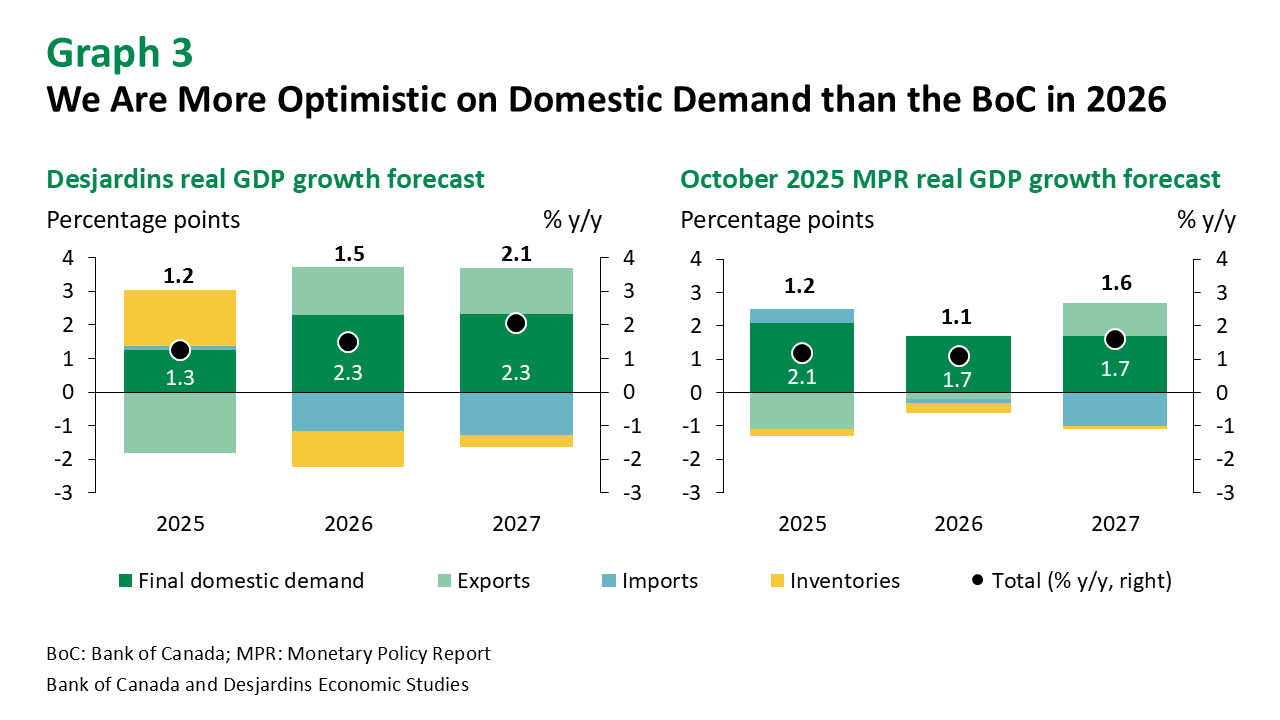

2025 Schedule of Central Bank Meetings